Rationale of the Deal

Thyssenkrupp is looking for new opportunities to put the group’s balance sheet in order again. An elevator unit IPO would aid much-needed restructuring and it would allow Thysenkrupp to consolidate the materials business. For Kone, who may not have enough financial capacity for a complete takeover, but a merger could work, this deal would yield the ultimate prize in the elevator industry, a giant installed base, specially after China’s residential-construction boom has slowed.

50% Chances of Approval

The parties present significant horizontal overlaps in new equipment and maintenance services for elevators and escalators and this may complicate an approval. A Thyssenkrupp-Kone elevator merger is unlikely to yield enough leverage to raise prices or squeeze rivals out in the new-equipment segment as regulators would likely define the market as being EU-wide. If so, EU regulators may allow a consolidation 4 to 3 as they did in the chemicals and telecom industries. The new equipment market for elevators and escalators is dominated by Otis, Kone, Thyssenkrupp and Schindler with about 80% EU market share.

In the maintenance market, the antitrust analysis may be more negative for the parties as regulators may defined the market nationwide. That means that the merged entity could dominate some markets in central and Eastern Europe and raise prices or try to squeeze smaller competitors out.

Divestitures may affect the rationale of the deal

If the two companies strike a deal, they will likely need to offer concessions in maintenance and modernization services to appease regulators. The problem is that the scope of the remedies, as in Siemens-Alstom and in Thyssenkrupp-Tata, may be too high for the companies to accept. Yet, the companies may be willing to accept a “loss” in Europe to capture a bigger market share in the Chinese market.

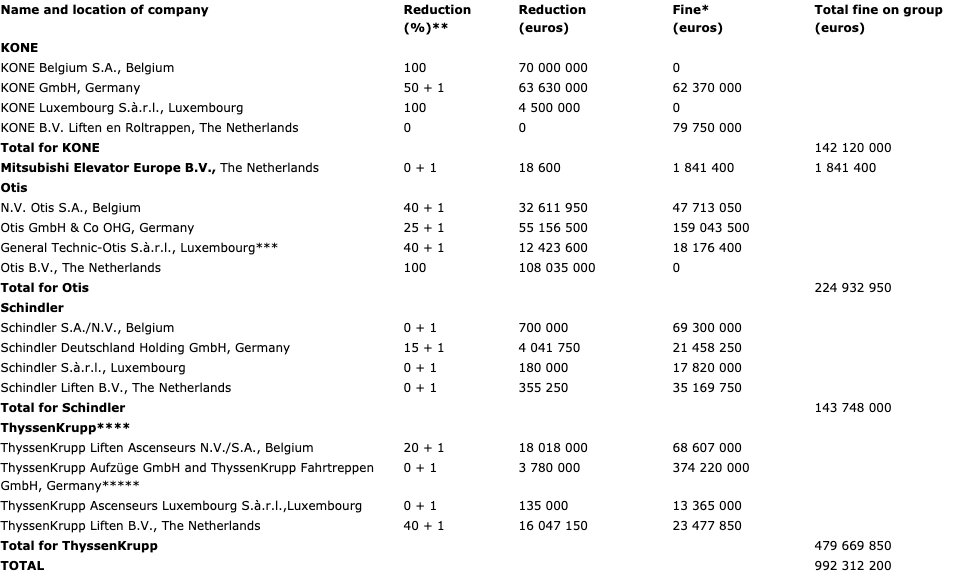

Risk of collusion may complicate an approval

Precedents of collusion among the four leading companies would likely raise regulator’s concerns about the risk of this practices being engaged again, given the industry’s price stability and the slow pace of growth in Europe. The four companies were fined about $1 billion in 2007 for rigging public tenders and other contracts for the sale, in the installation and servicing of elevators and escalators in Belgium, Luxembourg and the Netherlands.

The merger review would last until 2020

A potential tieup between the two companies would likely need an in-depth review by EU regulators. This would push back any possible decision to 2020. EU regulators would likely open a second phase merger review, and given the complexity of the deal and the need to craft adequate remedies, deadline extensions and suspension could also be expected. In addition to the EU approval, the parties would require regulatory clearances from the U.S., China and several other countries before being able to close the deal.