Visa and Mastercard may face more antitrust scrutiny in Europe if they were to expand to new business areas than other PayTech competitors like Paypal, Worldline or Nexi. In the latest antitrust decisions in Europe, Mastercard-Nets, Worldline-Ingenico and in the U.K., Paypal-iZettle and Visa-Plaid, regulators have started to defined markets more narrowly, have raised more concerns and have paid more attention to the concept of “potential competitors”. But probably you want to know what this means for companies. Alright, let’s put these changes in context.

Paypal, Worldline Could Still Resort to M&A

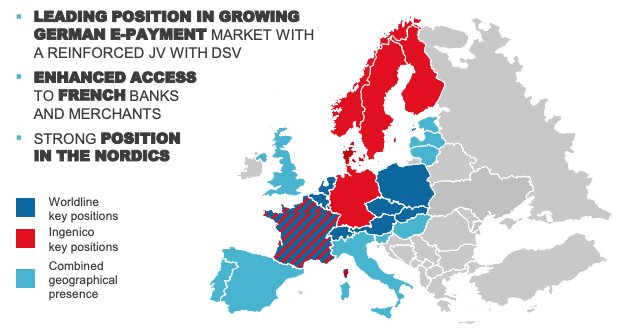

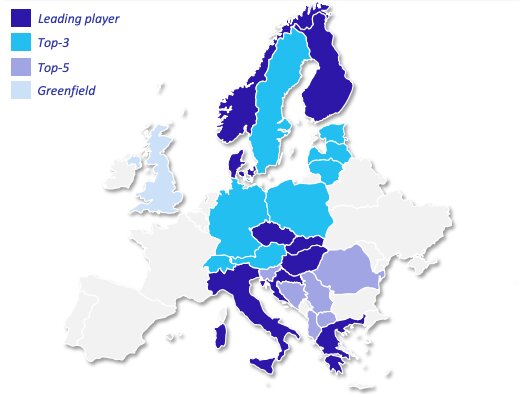

Paypal, Worldline, Worldpay and other companies active in point-of-sale (PoS) and mobile PoS businesses may still have room to expand via M&A in Europe, but they shouldn’t be surprised if any potential deal in these areas is subject to antitrust scrutiny and possibly remedies. Worldline’s CEO stated in the last earnings call that the company won’t pay dividends to have enough resources for new potential M&A, even if the company is still completing Ingenico’s deal. The PoS payment segment is probably one of the most predictable market in fintech from an antitrust point of view. Regulators apply a rather traditional antitrust analysis based on market shares and barriers to entry. For instance, in Paypal-iZettle and FIS-Worldpay M&A the companies dodged divestitures because there were many competitors in the U.K. market, but in Worldline-Ingenico, the levels of concentration in central European countries were higher and the parties had to divest. Thus, market shares may dictate the fate of new M&A, which is good news for most of the companies given the fragmentation of the payment industry in Europe. Yet, companies with a strong foothold in one member state, Worldline (France), Nexi (Italy), may only be able to expand geographically to areas where they have no presence.

Nexi-SIA-Nets May Also Get Away With Merger

Merchant acquiring services is the second-most predictable fintech market, in our view, but it may also face scrutiny. Most of the deals involving this market cleared without remedies, but regulators are raising some flags as the market is clearly in a consolidation phase. To this end, as we said before, most of the deal cleared without remedies, but not all. In Worldline-Ingenico, the parties had to divest the merchant acquiring business in Luxembourg. These markets are usually defined nationally, given language, technical and legal requirements to establish relationships between financial institutions and merchants. As a result of the geographically narrow market definition, it is possible that future M&A will raise concerns at this level, like Nexi-SIA-Nets could have in Italy. We wouldn’t be suprised if as a result of the consolidation in the market (Global-TSYS, Worldline-Ingenico, FIS-Worldpay), regulators will be more strict.

Visa, Mastercard May Have to Rethink Strategy

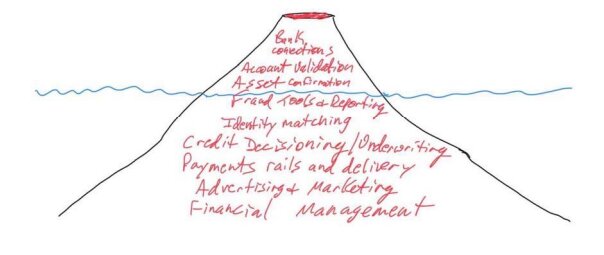

Visa and Mastercard seem to be particularly interested to expand to a new business line, Account-to-Account (A2A) payments, but they may face an uphill road if they try via acquisitions. Regulators are wary that card companies will try to suppress a nascent technology that could compete with the card-based payments schemes. A2A payments allow fintech companies to connect consumers and financial institutions without the need of a credit or debit card. Funds are directly subtracted from the user’s bank account and go directly to the merchants account. This technology is faster, cheaper and to certain extend more secure that using card networks. Visa’s Vice President of corporate development and Head of Strategic Opportunities defined Plaid as “an island “volcano” whose current capabilities are just “the tip showing above the water” and warned that [w]hat lies beneath, though, is a massive opportunity – one that threatens Visa”.

In our view, A2A is the least predictable fintech market from and antitrust angle and the fate of future M&A is still uncertain. In Mastercard-Nets, EU regulators requested the parties to divest Net’s A2A business. In Visa-Plaid, while the U.K. regulator approved the deal, ultimately blocked by DOJ, it stated that A2A is growing rapidly and will compete with card-based payments very soon. The only reason why the deal wasn’t blocked in the U.K. was the existence of other competitors in the market.

Most M&A Will Clear, But Few will Raise Flags. More Time To Review

The European payment market is still very fragmented and companies are in a race for consolidation. In our view, there is still plenty of room for consolidation and many of the future combination will likely secure regulatory approvals. Yet, in some of the segments mentioned above, we already see a few players of relevant size, and any plan to acquire a company will likely be subject to antitrust scrutiny in Europe. This includes the big tech companies, if they try to enter or expand in the payment sector through M&A.

In terms of timing, antitrust regulators may also need more time to review upcoming deals as markets become more concentrated, market definition may still evolve and the technology is rapidly changing. Products will be key to determine which deals may be anticompetitive. In short, fintech M&A will be an interesting industry to follow in the next months or years where EU companies are trying to gain scale and scope to better compete with U.S. rivals.