Stock exchanges across Europe, including Swiss SIX and Deutsche Borse have shown interesting in acquiring Borsa Italiana and its bond trading platform, MTS, but it is the Franco-Dutch exchange Euronext the best positioned and most interested as this acquisition could boost its earnings up to 30%, according to Morgan Stanley.

Rationale of the Deal

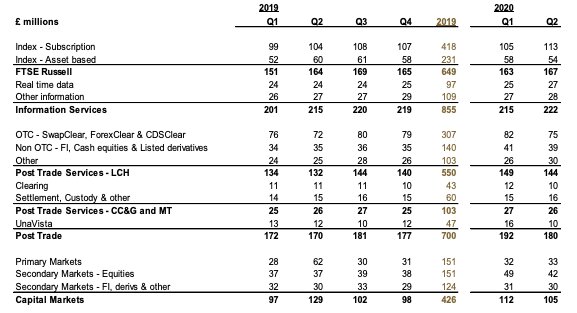

The London Stock Exchange is seeking to acquire data provider Refinitiv for $27 billion to create a powerhouse that will combine LSE’s trading venues and clearing houses with Refinitiv’s financial data products. The acquisition will shift LSE’s business portfolio further towards fast-growing data, analytics and index services to compete more efficiently with U.S. exchanges and financial data providers like Bloomberg.

Concerns May Be Addressed With Disposals

After the preliminary assessment, European regulators raised concerns in four markets: 1) Electronic trading of European Government Bonds, 2) Trading and clearing of Interest-Rate Derivatives 3) Consolidated real-time datafeeds and desktop solutions and 4) Index Licensing. The first two refer to market infrastructures and divestitures may be the best remedy to mitigate these concerns. This would include the sale of MTS or Borsa Italiana, LSE’s main venue for trading European Bonds. Alternatively, the parties could sell Refinitiv’s Tradeweb bond platform, but this platform showed a higher growth in the last years and it it has a more diversified geographical footprint, with more than half of its revenue coming from the U.S. The last two concerns refer to the risk for third parties (competitors of either LSE or Refinitv) of losing access to financial data. This type of concern could be addressed with behavioural remedies where third parties could still get access to LSE’s Russell Indexes and Refinitiv’s datafeeds after the deal.

Chances of Approval Are Higher Than Precedents

Since the companies are poised to dispose assets to appease regulators the deal’s approval may not be at risk. Additionally, unlike previous failed attempts by LSE and other exchanges to merger, this deal doesn’t raise any politically sensible issue and the only possible one, too much power over the electronic trading of European Government Bonds will likely be solved through divestiture. The second biggest risk for the companies after the horizontal overlap in trading of European Bonds is the vertical concerns over financial data inputs. While the companies may be prepared to offer some behavioural remedies in this area, a tougher approach by regulators requiring divestitures of the highly profitable LSE’s Russell indexes or some datafeeds, could derail the transaction, but this isn’t likely.

Approval May Slip Into 1Q21

The decision by the European Commission could be issued by year end, but after the latest deadline suspension on October 27, the approval may be pushed back to 1Q21. The review is currently halted until the parties submit the information requested by regulators. If the review resumes in the first half of September, a new deadline for a decision may be established in mid December, but any deadline extension either for new data request or simply because the parties submit remedies to appease regulators, it will likely push the statutory deadline to January. New deadline suspensions or extensions can’t be ruled out.