In January 2026, Edwards Lifesciences officially terminated its $945 million acquisition of JenaValve Technology after a U.S. District Court granted the FTC a preliminary injunction. The deal was particularly interesting from a legal perspective for two reasons: the FTC used clinical data to prove that the merger would create a “pre-commercial monopoly” in the nascent market for heart valves designed to treat aortic regurgitation (TAVR-AR), and the evidence the FTC needed to challenge the deal was found in Edwards’ own 10-Q report.

A Deal That Was Actually Two

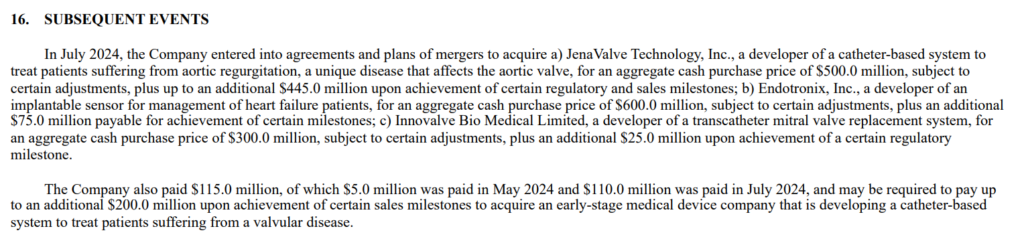

In July 2024, Edwards Lifesciences announced an agreement to acquire JenaValve Technology. The deal was designed to expand Edwards’ portfolio by adding JenaValve’s Trilogy Heart Valve System.

However, the merger faced an immediate challenge from the Federal Trade Commission (FTC) for the following reasons:

- Pipeline Monopoly: The FTC argued that the deal would create a “pipeline monopoly” because it combined the only two companies with ongoing U.S. clinical trials for transcatheter AR (TAVR-AR) devices.

- The “Stealth” Acquisition: Just days before the JenaValve announcement, Edwards had quietly acquired JC Medical, JenaValve’s only direct rival in the U.S. clinical trial space. The FTC characterized this as an “attempt to buy the U.S. market.”

On January 9, 2026, after a six-day trial, the U.S. District Court for the District of Columbia granted the FTC a preliminary injunction. The court agreed that the merger would likely “substantially lessen competition” in a market for research and development, even though neither device had yet received FDA approval. Following the ruling, Edwards officially abandoned the acquisition.

The Double Acquisition Hidden in Plain Sight

JenaValve and JC Medical were the only two companies in the United States conducting clinical trials for TAVR-AR devices. Edwards Lifesciences, the dominant incumbent in standard TAVR, sought to acquire both startups. By acquiring both entities over the course of two days in July 2024, Edwards engineered a classic 2-to-1 “merger-to-monopoly.”

The FTC’s expert calculated that this dual acquisition would drive the Herfindahl-Hirschman Index (HHI) for U.S. clinical trial sites from 5,356 to a perfect monopoly score of 10,000, rendering the deal structurally indefensible under Section 7 of the Clayton Act. However, the FTC’s true masterclass was in how it weaponized Edwards’ own financial documents to prove anticompetitive intent.

The FTC’s litigation strategy focused on the discrepancies in Edwards’ earlier Form 10-Q filings to establish anticompetitive intent. In that filing, Edwards explicitly announced its $945 million agreement to acquire JenaValve. Yet, in the exact same 10-Q, Edwards deliberately anonymized its simultaneous acquisition of JC Medical, referring to it vaguely as “an early-stage medical device company that is developing a catheter-based system.” Furthermore, the SEC filing omitted any mention of Edwards’ concurrent $25 million investment in JC Medical’s parent company, Genesis MedTech.

The FTC argued, and the District Court agreed, that Edwards’ differential reporting in its SEC filings was a calculated move to execute a stealth consolidation of the pre-commercial TAVR-AR market.

This regulatory maneuver successfully blindsided JenaValve’s leadership, who testified they “more than likely” would not have agreed to the Edwards merger had they known Edwards had secretly acquired their only U.S. clinical competitor one day prior. Under antitrust jurisprudence, this behavior strongly evidenced “unilateral effects” and a deliberate strategy to eliminate head-to-head innovation rivalry, violating the Clayton Act.

Engineering an Acquisition Below Notification Thresholds

If hiding the acquisition in the 10-Q partially showed an intent to monopolize, the deal structure was the ultimate evidence of this intent.

Edwards deliberately priced the upfront acquisition of JC Medical at $115 million (finalized at $116.3 million net) alongside an additional $200 million in contingent milestone payments. This valuation was surgically positioned just below the $119.5 million Hart-Scott-Rodino (HSR) Antitrust Improvements Act reporting threshold.

The 10-K also disclosed a $75 million promissory note advanced to JenaValve to sustain its operations while the merger was under regulatory review. By structuring the JC Medical deal below the $119.5 million HSR threshold and obscuring the target’s identity in its 10-Q, Edwards bypassed mandatory pre-merger antitrust notification. The FTC used this exact data point to show the court that Edwards intentionally engineered the JC Medical valuation to bypass mandatory pre-merger antitrust notification, facilitating a stealth roll-up of the market.

Conclusion

The financial mechanics and SEC reporting discrepancies proved fatal to Edwards’ antitrust defense. The FTC did not merely look at the 10-K to understand the deal’s economics; it used the timeline of the 10-Q disclosures to build a narrative of corporate subterfuge. By proving that Edwards engineered a sub-HSR valuation for JC Medical and utilized vague SEC reporting to conceal a simultaneous roll-up of the U.S. TAVR-AR clinical pipeline, the FTC demonstrated an irrefutable intent to monopolize.