The UK’s Competition and Markets Authority (CMA) launched its Phase II investigation on the $3,700 million Getty–Shutterstock merger on November 3. Meanwhile, the U.S. Department of Justice is also reviewing the deal.

As expected, when the regulator opened a Phase II (second-stage) merger review, the stock took a hit. That’s natural—but it doesn’t necessarily signal new concerns. In many cases, the authority simply needs more time to assess the evidence. When the sell-off is sharp, it can create an attractive entry point. That’s how we did a +11% in a few hours.

Our preliminary analysis suggests both Getty and Shutterstock may be undervalued. That said, in a sector facing heavy AI-driven disruption, they could also be value traps. The reason why they moved from our watchlist to our portfolio is because the regulatory news caused an unjustified drop. Besides, if the antitrust issues are resolved, the combined group could gain quasi-monopoly advantages—an edge worth considering even in a market being reshaped by AI.

What’s the Deal?

Getty Images and Shutterstock—two of the world’s largest providers of stock and editorial photography—agreed on January to merge. The deal value is around $3,700 million, the combined annual revenue is nearly $2,000 million and the parties expect to obtain annual cost synergies around $150-200 million.

One of the main purpose, if not the only one, is to consolidate assets and compete in an increasingly AI-driven media landscape, particularly in areas like generative content, video, and metadata-rich image licensing.

This is not just a merger of two content libraries. It’s a defensive strategic bet to remain relevant in a market where generative AI is threatening the traditional business model of image licensing.

What’s at Stake?

This deal comes at a critical moment for both companies. Getty Images, despite its premium brand and exclusive editorial deals, faces rising costs and the erosion of licensing value due to generative AI models. Shutterstock has maintained solid market performance but is also under pressure as customers increasingly generate content in-house with AI tools.

On July 29, Shutterstock reported strong second-quarter results, posting year-over-year growth in both revenue and adjusted EBITDA. Adjusted EBITDA rose 32% to $82.2 million, with margins improving to 30.8%, up from 28.2% a year earlier. Revenue from the company’s Content segment reached $199.8 million, up 18% YoY, while its Data, Distribution, and Services segment saw a 34% jump to $67.2 million.

Commenting on the Company’s performance, Paul Hennessy, the Company’s Chief Executive Officer, said, “I am pleased to report that Shutterstock set new high water marks in the second quarter, achieving record levels in both Revenue and Adjusted EBITDA. Our complete suite of offerings, from creative content to custom creative solutions to AI model inputs to our GIPHY distribution is now more than ever enabling us to fuel great work for our customers.

The company’s strong results suggest not only growing revenue and profits, but also that Shutterstock may be well positioned to navigate the AI-driven disruption reshaping the industry. While this is encouraging for investors, it could complicate the legal arguments underpinning its merger filing with Getty. Specifically, it may become harder to claim that the deal is essential for survival in the face of AI challenges—an argument that could be central given that the combined entity would likely control over 50% of the market and face significant regulatory scrutiny.

Some analysts, however, are more cautious. They note that the earnings beat may have been driven by a one-off data licensing deal, pointing out that Data, Distribution, and Services (DDS) revenue surged 69% quarter-over-quarter, while Content revenue actually declined 1.5% during the same period. If this is true, Shutterstock could still explanin why the deal is necessary to survive, it won’t please investors, but may appease regulators.

Analysts’ View on Shutterstock-Getty:

- Wall Street has largely welcomed the merger, seeing potential for cost synergies, pricing power, and a stronger AI licensing platform.

- But there’s risk: demand for traditional image licensing is falling. Generative AI platforms (including those powered by Stability AI, OpenAI, and Midjourney) are displacing large volumes of creative imagery.

- Many analysts have recently lowered their price target for Getty Images although they maintain their “buy” ratings.

- Both companies are pivoting fast—Getty launched a generative image tool (in partnership with Nvidia), while Shutterstock works with OpenAI and Google.

What’s the Antitrust Risk?

In the UK, looking at precedents—most notably the Getty–Rex case—the regulator is expected to define multiple relevant markets: stock images, editorial images (including entertainment, news, and sports), archive imagery (which is non-replicable and often exclusive), and potentially a new category: AI-enabled content and training data.

While we lack precise UK-specific market share figures for each segment, Getty and Shutterstock together control probably around 50% of the global stock image market. In editorial submarkets, especially in the UK, their combined share may be even higher.

Holding 50% of any market would typically trigger regulatory scrutiny—but what compounds the concern here is the lack of credible alternatives. The rest of the market is highly fragmented, with smaller competitors lacking the scale, distribution, or exclusive access needed to exert meaningful competitive pressure on the merged entity.

Competitors:

- Adobe Stock, Alamy, Depositphotos, and 123RF provide partial overlaps in stock.

- Reuters, Associated Press, and EPA Images are active in editorial.

- No single competitor offers the same scale, global distribution, and combination of editorial + stock.

That asymmetry could make it hard for smaller agencies to constrain the merged firm—especially as AI training data becomes a key asset.

The role of AI will be central to the merger review. On one hand, generative AI poses a significant threat to both companies, as many media agencies are turning to in-house AI tools or alternative image-generation partners, reducing their reliance on traditional stock libraries. On the other hand, Getty and Shutterstock are actively investing in AI partnerships, using their vast image archives to generate new content, provide legal certainty, and compensate creators. This approach could prove especially valuable for large agencies and corporate clients seeking high-quality visuals without the risk of copyright disputes or litigation—a key differentiator as legal scrutiny around AI intensifies.

Will It Be Cleared?

It is not guaranteed. In the UK, a Phase 2 investigation doesn’t mean the regulator found significant new concerns. But in this case, the parties tried to fix the concern during the phase one with some remedies, and the regulator didn’t accept them yet.

Regulators will need time to understand how AI tools, training data access, and exclusive content rights interact in this new market structure and if they could offset the potential market power that the combined entity could have.

That said, the CMA has adopted a more company-friendly tone in recent reviews, and outright blocks have become less common. A key in the analysis will be whether AI will lower the barriers to entry in some of these markets or not. If the regulator finds that the deal will raise competition concerns, it could also seek remedies from the parties like structural remedies, e.g., divestment of overlapping assets or mandatory licensing of image data—including for AI training.

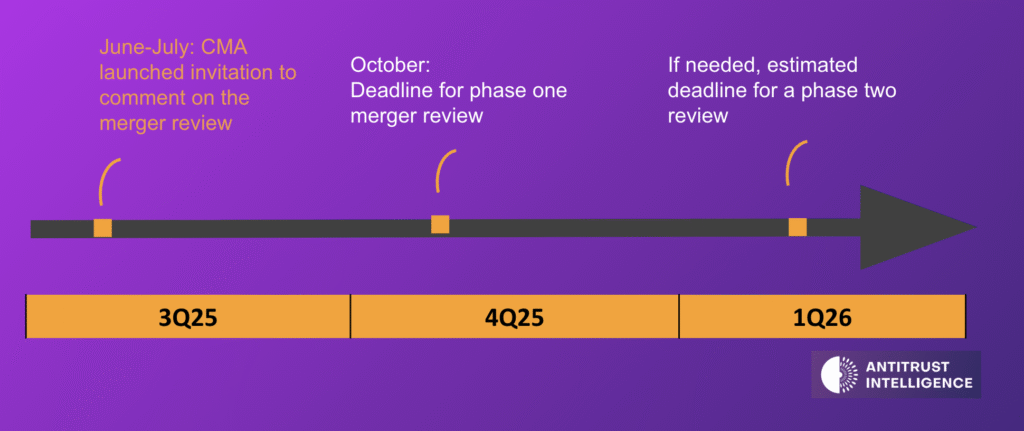

What’s the Timeline?

The statutory Phase 1 deadline was October 20. The new statutory deadline for a Phase 2, is April 19, 2026. The parties may skip the filing before the European Commission, because their revenue may not reach the notification thresholds in Europe.