The Competition and Markets Authority (CMA) has concluded its extensive investigation into the UK’s £6.7 billion veterinary services market, finding that the current system is failing pet owners, who have seen prices rise by 63% since 2016. To address these issues, the regulator is mandating a “fundamental reset” of the industry through legally binding orders.

A primary focus of the new requirements is transparency of ownership and pricing. Currently, six large corporate groups own 60% of UK practices, yet many consumers are unaware their local vet is part of a major chain. Moving forward, all practices must clearly disclose their corporate parent on signage and websites. Additionally, vets will be required to publish prices for a standard list of common services, such as consultations, vaccinations, and health checks, to allow for easier consumer comparison.

To protect consumers from “bill shock” during high-stakes medical situations, the CMA is introducing mandatory written estimates for any treatment likely to exceed £500. Practices must also provide itemized billing and ensure that clinical staff can provide impartial advice without being swayed by corporate targets or internal commercial pressures.

The remedies also take aim at the high cost of medicines, which are often significantly cheaper online than at a clinic. Vets must now explicitly inform owners that they have the right to a written prescription to shop elsewhere. To ensure these prescriptions remain accessible, the CMA is capping the fees for these documents at £21 for the first item and £12.50 for subsequent ones.

Quick Review Table: CMA Veterinary Remedies

| Category | Key Remedy | Specific Requirement |

| Price Transparency | Standardized Price Lists | Practices must display prices for common services (consultations, scans, neutering, etc.) on websites and in-clinic. |

| Business Ownership | Mandatory Disclosure | Signage and websites must clearly state if a practice is part of a large corporate group. |

| Treatment Costs | Written Estimates | Vets must provide a written cost estimate for any treatment pathway likely to cost £500 or more. |

| Billing | Itemized Invoices | Bills must be broken down by service so owners can track charges and identify errors. |

| Medicines | Prescription Fee Caps | Fees for written prescriptions are limited to £21 (first item) and £12.50 (additional items). |

| Medicines | Online Savings Awareness | Vets must inform owners that medicines may be cheaper online and provide prescriptions promptly. |

| Complaints | Mediation Access | Practices must have a formal in-house complaint process and engage in mediation if requested. |

| Cremations | Service Options | All practices must offer lower-cost communal cremation as an alternative to individual services. |

| Out-of-Hours | Contract Flexibility | Providers cannot use termination periods longer than 12 months, making it easier for practices to switch. |

For a full list of remedies, you can consult the CMA’s market study.

Impact on Clinics

All measures are likely to have an economic impact on clinics, ranging from the administrative burden of itemizing bills to the capital expenditure required for website updates. However, the factors likely to exert the most significant pressure are the prescription fee caps and the heightened scrutiny of upselling practices.

By capping written prescription fees at £21 for the first medicine and £12.50 for any additional items, the regulator is effectively dismantling the “hidden subsidy” model that has defined the industry for years. Historically, many clinics suppressed consultation fees by applying high markups to medications; the new cap forces a decoupling of these costs, ensuring that pet owners are not financially penalized for choosing to procure medications from online pharmacies. Essentially, clinics prefer to sell pharmaceuticals rather than prescriptions.

For a firm like VetPartners, where “Drugs” and “Other Sales” contribute significantly to a 77% gross margin, this represents a material threat. If even 25% of current in-practice medication volume migrates online, the impact on practice-level EBITDA could be substantial.

For pet owners, the impact is immediate transparency and significant savings. However, for clinics, this cap is a double-edged sword. To recoup the margin lost from high-margin medicine sales, many providers may be compelled to increase the pricing of their professional time and clinical expertise. Consequently, while prescriptions may become more affordable, consumers may see a corresponding rise in consultation fees and surgical costs as clinics transition toward a “fee-for-service” model that more accurately reflects the high overhead of modern medical facilities.

CVS Group (CVSG) have informed investors that they were already compliant with most CMA remedies and expect minimal impact. Simultaneously, however, the company is expanding in Australia, cognizant of growth limitations in the UK. Investors appear less comfortable with the remedies.

The Structural Risks of Private Equity Ownership

Private equity (PE) firms buy veterinary clinics because they offer steady cash flows, healthy margins, and a resilient customer base.

The model is straightforward: the PE firm typically seeks an exit within three to seven years. Firms acquire small practices from retiring veterinarians at low multiples (e.g., 5x profit) and aggregate them into a larger group. They then seek to sell the consolidated entity to a subsequent PE buyer or via the public markets at a higher multiple (e.g., 12x profit). For example, EQT Partners acquired IVC Evidencia in 2016, expanded across Europe, and is currently preparing for an initial public offering (IPO).

When a PE firm acquires a clinic, it rarely utilizes its own capital for the entire purchase, typically employing 70%–90% debt. Crucially, this debt is not held by the PE firm itself; it is “pushed down” onto the balance sheet of the portfolio company.

By burdening the veterinary group with substantial interest payments, the group’s taxable profit is effectively neutralized. In the UK, interest payments on business loans are often tax-deductible. Therefore, a clinic generating £1M in operating profit might pay £1.1M in interest to a lender, frequently an entity related to the PE firm, resulting in a £100k loss reported to HMRC and zero Corporation Tax liability.

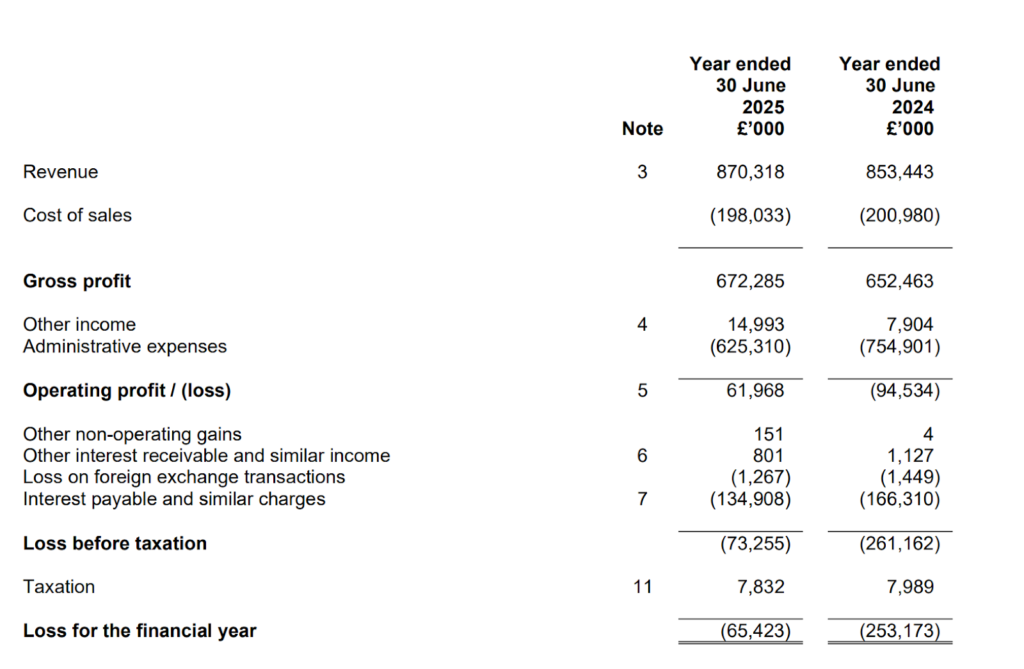

VetPartners’ Annual Accounts 2025

The underlying risk is now evident: following the CMA’s remedies, clinics may experience a yet-to-be-quantified impact on revenue, while the debt service obligations to lenders and parent companies remain fixed. Profitability metrics, such as Return on Capital Employed (ROCE) versus Weighted Average Cost of Capital (WACC), may suggest healthy performance, but this “fabricated profitability” often excludes critical financial realities.

While the PE sponsor intends to sell to a subsequent buyer, valuations may now face downward pressure. For sponsors like BC Partners (owners of VetPartners), the market study has already complicated the exit environment. Potential acquirers may be wary of an asset facing restricted acquisition growth, limited upselling opportunities, and long-term revenue headwinds. If future buyers cannot rely on organic revenue growth, they may pivot toward aggressive cost-reduction strategies, including the closure of underperforming clinics.

Market Intelligence and Legal Opportunity

Beyond the long-term effects on PE funding, this market study creates significant opportunities for law firms to advise both PE sponsors and their portfolio companies.

CMA Compliance and “Readiness” Audits Large groups (but also small clinics) must implement a wide-ranging package of transparency measures by late 2026. Law firms can offer:

- Signage and Digital Audit Services: Ensuring hundreds of disparate sites comply with mandatory ownership and price disclosure rules to mitigate the risk of CMA enforcement action.

- Policy Drafting: Developing the written policies now mandated by the CMA to safeguard clinical staff from commercial pressures. A “tug of war” between management and veterinary staff regarding these policies is anticipated.

- Complaint and Mediation Programs: Assisting firms in establishing the required in-house mediation processes to resolve consumer disputes.

Transactional Due Diligence 2.0: “The CMA Risk” Standard due diligence checklists are no longer sufficient. Advisors should focus on:

- Revenue Quality Assessments: Analyzing the percentage of target EBITDA derived from medicine mark-ups versus professional fees to quantify the impact of the prescription fee cap. PE firms may require comprehensive portfolio valuation reviews.

- Local Concentration Analysis: Utilizing the CMA’s “FTE vet share” methodology to assess whether proposed bolt-on acquisitions will trigger merger investigations or mandated divestments.

- VSA Pre-Compliance: Auditing targets for readiness under the forthcoming mandatory licensing regime.

Regulatory Defense and Public Policy Advocacy As the RCVS gains new monitoring powers funded by a site-specific levy (£450–£550 annually), the frequency of regulatory friction will likely increase. Law firms can provide:

- RCVS Disciplinary Defense: Representing corporate entities in the new “fitness-to-practice” cases that will inevitably arise.

- Lobbying and Consultation Support: Representing the interests of Large Veterinary Groups (LVGs) during the drafting of the new Veterinary Services Act to ensure the resulting legislation remains operationally viable.