In March 2024, Bondalti Chemicals launched an unsolicited takeover bid for Spanish chemical company Ercros—the second such offer for the company, following a competing bid by Italian group Esseco, which we also analyze here. While the Portuguese competition authority (AdC) cleared the deal without conditions in June 2024 , Spain’s CNMC initiated a second-phase investigation, highlighting notable differences in regulatory scrutiny.

Main Antitrust Concerns in Spain

According to the CNMC, the Bondalti/Ercros deal raises significant concerns in two key product markets: sodium hydroxide (caustic soda) and sodium hypochlorite (bleach). The two companies are among the largest producers in the Iberian market, and their merger would result in a combined market share exceeding 50% in caustic soda and up to 70% in sodium hypochlorite in Spain.

The CNMC emphasized several competition risks: the remaining competitors are relatively small and may not exert sufficient pricing pressure; imports of caustic soda, while present, are considered unreliable due to volatile transport costs and infrastructure limitations; high barriers to entry, especially the need for specialized plants and storage infrastructure; and potentially higher prices for customers, because Ercros has the capacity to set prices for the industry.

Because of these factors, the CNMC referred the case to an in-depth second phase, signaling that approval will likely require significant remedies or risk prohibition.

The More Lenient View in Portugal

In contrast, the Portuguese Autoridade da Concorrência (AdC) approved the merger without imposing any remedies. The AdC’s analysis, published in June 2024, emphasized several mitigating factors: the parties’ overlaps in Portugal are relatively modest; soda caustica is considered a homogeneous commodity product, easily tradable across borders; over 50% of caustic soda consumed in Portugal is already imported, demonstrating robust external supply alternatives; transportation costs for caustic soda are low, facilitating cross-border competition; and market feedback confirmed that alternative suppliers exist both within and outside the European Economic Area (EEA).

In short, the AdC concluded that the deal would not significantly harm competition because of the strength of import competition and the standardized nature of the product.

Spain Has a Different View

Despite the concerns in Spain, several factors could still work in Bondalti’s favor during the CNMC’s second-phase review—potentially tipping the balance toward conditional approval with remedies rather than outright prohibition.

First, the EU precedents cited by the Portuguese authority to support clearance could also be invoked in Spain to argue for broader market definitions—at the EU or even global level. If the CNMC adopts a wider geographic market, the merged entity’s market share would be significantly lower, making it more difficult for the regulator to establish market power. Notably, the Spanish authority has already acknowledged the possibility of defining the relevant market at a European level.

Second, both caustic soda and bleach are highly commoditized products, which facilitates supplier switching by buyers whenever pricing or supply conditions worsen. Moreover, many of the key customers are large industrial groups that possess strong negotiating power, often capable of diversifying their supplier base.

Additionally, while not as robust as in Portugal, the Spanish market also benefits from import competition. Transportation costs for caustic soda are relatively low compared to the final product price, and even if there are some limitations about how far the product could be transported (around 400KM), it is feasible for Spanish buyers to source from neighboring European countries. Should local prices rise excessively, buyers could turn to foreign suppliers to reintroduce competitive pressure.

The Spanish regulator acknowledged that, while imports currently play a limited role due to lower domestic prices, this dynamic is evolving. Following the closure of one of Ercros’ production facilities, domestic supply has tightened, and Ercros’ customers increasingly rely on imports to meet demand. Although these imported alternatives may be more expensive, their growing role demonstrates that alternative sources do exist—particularly when market conditions shift—supporting the argument that the market is not fully confined to national boundaries.

Likely Outcome: Remedies Will Be Necessary

The reasons outlined above suggest that the parties could avoid an outright prohibition, but it remains unlikely that the CNMC would approve the Bondalti/Ercros merger without conditions. Unlike the Esseco case—where approval with behavioral remedies (or small divestitures) appears feasible—this transaction is more likely to require structural remedies, given the overlap in production assets and the extent of the market concentration involved.

Possible remedies could include divesting production capacity in Spain or Portugal, offering long-term supply contracts to competitors, guaranteeing access to import and storage infrastructure for third parties, and implementing specific protections for smaller buyers to prevent abuse of market power.

The Cost of Divestitures

Should the CNMC require Bondalti to divest significant assets in Spain, the economic attractiveness of the deal could be materially impacted.

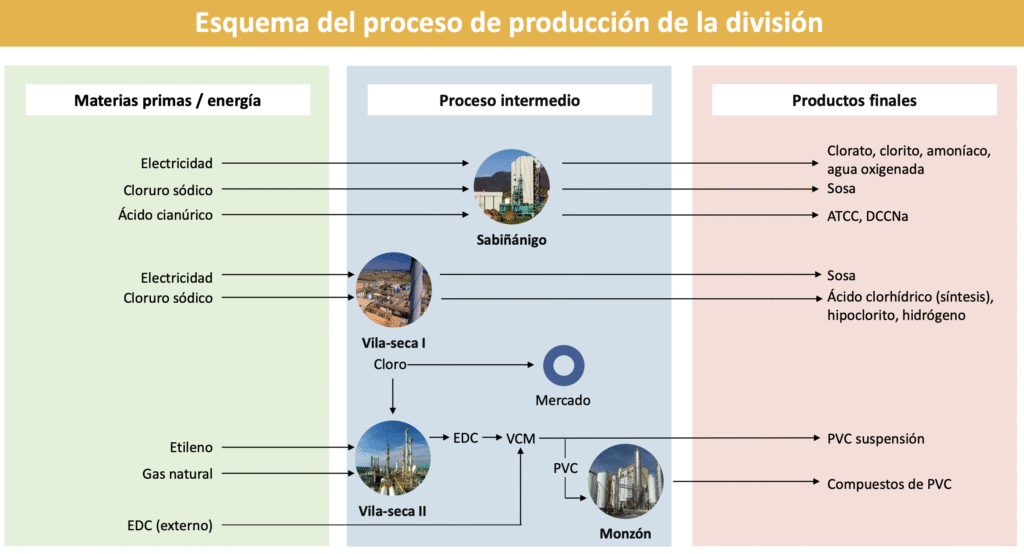

Much of the expected value of the transaction stems from synergies in production integration, logistics optimization, and commercial consolidation. Selling off production facilities would erode these synergies. If the parties need to sell assets, probably one of the factories from Ercros (Sabiñanigo o Vila-Seca) or Bondalti (Talavera) would be the likely target, but this would likely affect the company’s bottom line.

As a result, if Bondalti must part with a substantial share of Ercros’ Spanish operations, the anticipated cost savings and revenue enhancements could be cut significantly. This would not only reduce the financial upside of the acquisition but could also prompt a re-evaluation of the purchase price or the strategic rationale for proceeding with the deal under such burdensome conditions.