On May 16th, Microsoft submitted proposed remedies to the European Commission in an attempt to close the antitrust investigation into the potential abuse of a dominant position by tying Teams to its core SaaS productivity applications.

In this article, we explore how Microsoft crafted a remedy package that: 1) may appease regulators by ending the anticompetitive conduct and improving compatibility with third-party apps; 2) has little financial impact on Microsoft and is unlikely to affect its business in the long run; and 3) is probably not enough for Slack — but then again, no remedy would be.

What’s the Issue?

Following a complaint from Slack in 2020, the European Commission opened a formal investigation in 2023. It found that (i) Microsoft holds a dominant position globally in the market for Software-as-a-Service (SaaS) productivity applications for professional use, and (ii) since at least April 2019, it has been tying Teams to its core SaaS productivity applications, in breach of EU rules.

The Commission found that this conduct gave Teams an unfair distribution advantage reinforced by interoperability limitations between Microsoft’s products and rival offerings. In other words, Microsoft protected its dominance in productivity software and safeguarded its suites-based model from competitive pressure coming from standalone providers.

One point worth highlighting is that, in this fast-growing and still maturing market, establishing early dominance was key. As shown in the image below, Microsoft’s user growth skyrocketed during the period it bundled Teams with its SaaS suite — whereas growth before and after that period has followed a more linear trend.

Slack and Microsoft Teams users 2017 to 2023 (mm)

What are the remedies?

Under the proposed commitments, Microsoft would: (i) make versions of its productivity suites available without Teams and at a reduced price; (ii) allow customers to switch to these versions, even under existing contracts; (iii) offer Teams’ competitors improved interoperability with Microsoft products; and (iv) enable users to move their data out of Teams, making it easier to adopt rival services.

Arguably, these remedies put an end to the anticompetitive practice. They give consumers cheaper options, ranging from $1 to $8 depending on the version — coincidentally the discount matches the standalone price of Slack (€8). On top of that, Slack and other competitors would benefit from better integration with Microsoft tools.

At first glance, it will be hard for the European Commission to argue that these commitments are insufficient. It’s possible they may ask for clarifications to ensure smooth implementation — such as allowing users to switch or connect apps with a single click, without facing more friction than they would when using Microsoft’s own ecosystem. But these are implementation details, not flaws in the core proposal.

As for pricing, it’s a tough area to challenge as regulators don’t like to set prices. Microsoft is essentially offering users the choice between Teams or Slack for the same total price (under some Microsoft packages). That shifts competition to quality and user experience rather than cost. Any other pricing structure could unfairly push users away from Microsoft — or lock them in.

What’s the inicial reaction from Investors?

The overall impact appears negligible — and perhaps even slightly positive, as the move helps eliminate a legal risk and avoids further negative publicity.

At first glance, Microsoft’s stock price didn’t react to the announcement, suggesting that investors saw little financial consequence. The lack of immediate movement implies that the market had already priced in the outcome or simply didn’t consider it material to Microsoft’s bottom line. However, if we look at the stock’s performance in the week or month leading up to the announcement — a period when the remedy proposal may have been discussed privately with regulators or leaked — the share price saw a notable uptick. That said, much of that gain is likely tied to broader market optimism, particularly around Trump’s proposed changes to trade policy, rather than the antitrust commitments themselves. Still, analysts view Microsoft’s proposal as a smart step in clearing a long-standing issue with minimal cost.

What’s the impact for Microsoft?

Here’s where things get interesting. Let’s assume Microsoft had to choose between paying an antitrust fine or offering commitments that come with some cost.

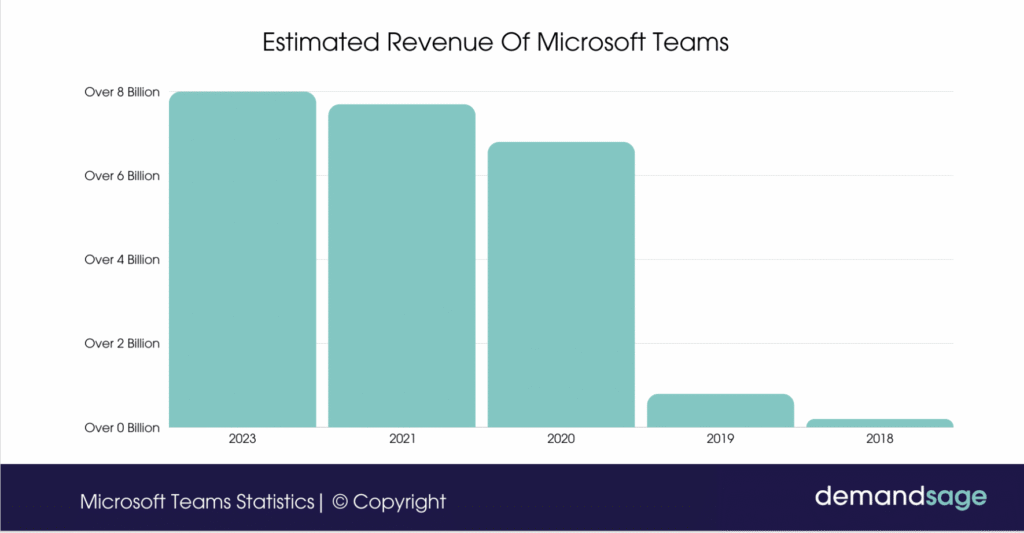

Technically, an antitrust fine can go up to 10% of a company’s annual global turnover — but for a company the size of Microsoft, and for this type of conduct, that’s unthinkable. A more grounded estimate would be to look at the revenue generated by Teams, which reportedly hit around $8 billion in 2023 — the year the EU launched its investigation.

Now, if the Commission were to fine Microsoft based on a portion of this $8 billion — say, 15% — the fine would come out to around $1.2 billion. On paper, that looks like a major penalty, especially for an abuse of dominance case. But in context, it’s barely a drop in the ocean compared to Microsoft’s $56 billion of free cash flow. Even a $2 billion fine, designed to include a stronger deterrent, wouldn’t move the needle financially.

Still, no one wants to write that check and still worry about litigation — so option B: offer remedies and close the case.

Now comes the real exercise: how many users will stop using Microsoft Teams simply because they opt for the cheaper version of Microsoft’s productivity suite — the one priced $1 to $8 lower?

As shown in the first graph, Microsoft Teams had around 320 million users in 2024 (including free versions and personal accounts). It is unrealistic to think that all users will just drop Teams for other options.

Once users have Teams installed and in regular use, there’s a natural sticking effect — especially in enterprise settings. Even if Teams isn’t the best product, organizations rarely switch away from tools embedded into their workflows, particularly when they’re tied to broader contracts and IT systems.

Also worth noting: while the remedies technically apply to the EU, Microsoft has said it will align its global suite offerings and pricing. So the risk of customer loss isn’t limited to Europe. Let’s say, conservatively, that 10% of business users drop Teams globally. That would translate into a $800 million revenue loss — at least in the first year.

On paper, a one-off fine — even a hefty one, like $2 billion — seems cheaper than losing $800 million annually, especially since lost customers are hard to win back. But in reality, a fine could come with tougher remedies down the line, potential divestiture risks, follow-on damages claims, and bad PR that might drag on the stock and hurt Microsoft’s position in future (and likely) investigations.

Was it Worthy?

If we take into account that Microsoft now makes around $8 billion a year from Teams (or in other words, around $30 billion from 2020 to 2023) and before the tying strategy, revenue from Teams was under $1 billion, the calculation becomes pretty clear. Taking the risk early on allowed Microsoft to tip the market in its favor, scale rapidly, and lock in users. Now, even if they have to face a fine or, more likely, accept remedies that barely scratch their financials, it was probably worth it.

And what about Slack (acquired by Salesforce)?

These remedies will probably cost Microsoft some customers — though it’s impossible to know how many. That said, they might actually help improve the 2025 guidance, especially as year-over-year growth is expected to slow. Still, it’s clear that these changes won’t rewind the clock to 2019, when Microsoft and Slack were competing head to head. That phase of the market is long gone.