On 16 July 2020, China’s SAMR cleared the JV created by Mingcha Zhegang (60%) and Huansheng Information (40%). This is the first merger officially accepted and unconditionally cleared by the Chinese competition authority, where a party was established using a Variable Interest Entity (‘VIE’) structure. In this case, Leading Smart Holdings Limited, a company registered in Cayman, controls Mingcha Zhegang through a VIE. The scope of the JV is technology, data process, development of artificial intelligence software and hardware and technical solutions to the catering industry.

After this decision, a VIE per se would no longer be a corporate structure that would allow companies, especially those in the internet industry, to escape the merger notification obligation in China, as it was the market practice so far.

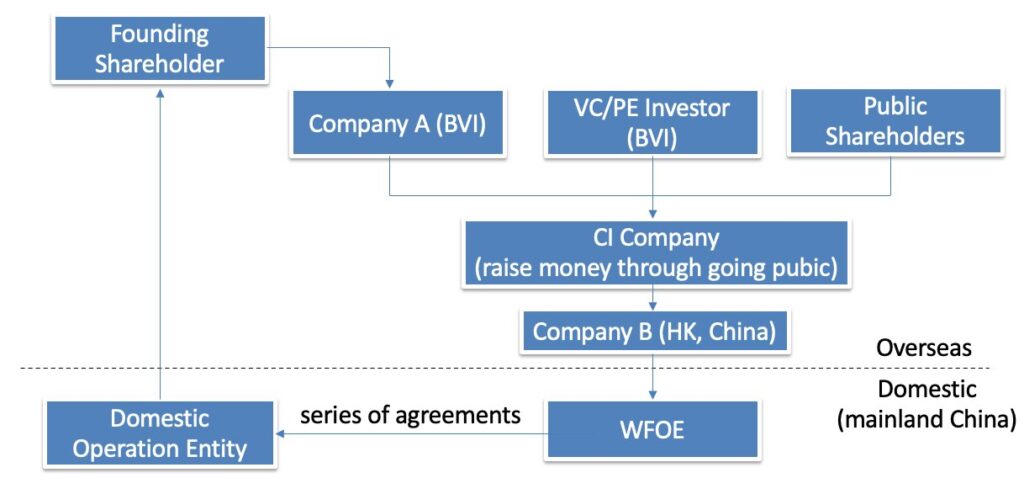

Not every VIE is established exactly with the same structure. Both BVI (British Virgin Islands) and CI (Cayman Islands) are famous for their attractive tax policies all over the world. WOFE refers to wholly foreign owned enterprises registered in mainland China. The domestic operation entity often comes from industries not totally open to foreign investors. Taking the internet-related industry as a typical example, foreign companies are prohibited from investing in internet news & information services, internet publishing services, internet audiovisual program services, internet culture operation (excluding music) and internet public information publishing services, unless certain sectors have already been open by China when it became a WTO member.

The WOFE controls operations, personnel, profit distribution, share issuance and stock option incentive of the domestic operation entity through series of agreements, such as asset operation control agreement, loan contract, equity pledge agreement, shareholder voting agreement, exclusive business cooperation agreement, etc. Through these agreements, the domestic operation entity would run under the control of the parent company – CI company. At the same time, the domestic operation entity obtains capital raised overseas.

VIE is a grey area in China. VIE has a history of around 20 years in China and almost all the internet titans, such as Alibaba, Tencent and Baidu, are beneficiaries of VIE. In early days, VIE was a convenient alternative for Chinese internet companies to raise money overseas, due to certain obstacles in the domestic market, but later it became very popular in almost all the industries.

The notification of a transaction involving a party that is using a VIE structure has always been a tricky question under China’s anti-monopoly law. On the one hand, there is not doubt that control obtained through VIE falls under ‘change of control’ in merger control and if the turnover condition is also met, the concentration should be notified. The Chinese competition authority has never denied that the AML requires notification in these situations.

However, the notifying party should make a commitment that their businesses and the notified merger are compliant with laws and regulations. The ‘grey area’ status of VIE prohibits the notifying party from making such a conclusive declaration. In 2009, Sina’s planned acquisition of Focus Media was dropped due to MOFCOM’s refusal to accept the case. There is also a concern that the Chinese competition authority’s acceptance and review of mergers concerning VIE might be misunderstood as ‘recognition’ and ‘endorsement’ of the legality of VIE.

In Walmart/Yihaodian case, MOFCOM separated VIE from the competition analysis. One of the remedies imposed was that Walmart was prohibited from engaging in the value-added telecommunications services run by Yihaodian. The transaction between Walmart and Yihaodian was read as an attempt by a foreign company to enter an industry not totally open to foreign investors through a merger. Yet, the remedy was lifted four years later in 2016, after relevant industrial restrictions were cancelled and foreign shares in online data & transaction processing services (business-oriented e-commerce) could reach 100%.

The biggest difference between Walmart/Yihaodian and Mingcha Zhegang/Huansheng Information is that in the latter Mingcha Zhegang has no connection with industries not totally open to foreign investors, in accordance with public available information. The Mingcha Zhegang/Huansheng Information decision means that future transactions concerning a VIE structure, which won’t aim to circumvent the law, will likely be reviewed by the SAMR.

Foreign companies would enjoy more freedom to invest in China, considering that sectors on China’s ‘negative list’ are reduced every year. Nevertheless, foreign companies seeking to use VIE to invest in industries not totally open to foreign investors, will likely face the same obstacles from the SAMR.

Image by Gerd Altmann from Pixabay