Commerzbank is Germany’s second-largest bank, with a strong footprint serving retail and large corporate customers across Germany. Yet, the high cost-to-income ratio of about 80% leaves the lender in a tough situation seeking a revenue uplift in the short term. Additionally, the bank is reducing its investment banking and financial service businesses. In this scenario, cost cuts seem to be the most likely route to boost profits. One way to achieve these cuts is through domestic synergies in a merger with Deutsche Bank. If this happens, what would antitrust regulators have to say about that?

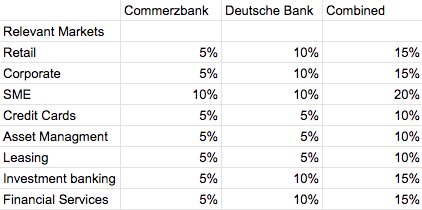

A Deutsche Bank-Commerzbank merger would’t face significant antitrust scrutiny given the combined market share in any of the relevant markets. The companies overlap in retail, corporate and SME banking, credit and debit cards, asset management, leasing, financial services and investment banking. Yet, Germany’s banking sector is highly fragmented and no bank enjoys a dominant position (not even close!). The parties aren’t likely to accumulate more than 15% of the market in any of the markets above-mentioned. SME banking may be an exception as the parties could have around 20%, a combined market share that is far from raising any antitrust concern, according to the EU precedents.

What about vertical or conglomerate effects? This is unlikely to be an issue. Commerzbank’s position in financial services in Germany isn’t strong enough to provide Deutsche Bank with leverage to engage in anticompetitive bundling or exclusionary practices. Deutsche Bank may be strong in the acquisition and trading of german bonds but adding Commerzbank won’t likely change that position. Besides, according to the EU precedents, most of the relevant markets in financial services and investment banking where this type of leverage could occur are normally defined EU-wide or worldwide. Thus, even if banks would engage in these practices, it would be difficult to sustain that they are anticompetitive.

Brexit may play out well for the German banks. It seems obvious that a deal of this scope should be filed in Brussels. Yet, under a “no-deal” Brexit scenario, the parties could skip the notification in Brussels and file the deal only in Germany. For a deal to have EU dimension, and therefore require a notification before the European Commission, the parties must generate their EU revenue in several EU countries. If the companies produces more than 65% of their EU-revenue in just one member state, the notification should be done in that member state. Commerzbank generates around 71% of its revenue in Germany and Deutsche Bank would generate around 72% of its EU-revenue in Germany if the U.K. isn’t included for these purposes after Brexit. An EU approval seems likely but an approval only from German regulators may be even easier to get.

In conclusion, Deutsche Bank and Commerzbank may have an easy antitrust path for approval, but the real challenge remains. Would they be able to achieve through the merger the synergies (cost cuts) that they desperately need? With strict labour laws in Germany that restrict job cuts, the questionable US adventure of Deutche Bank and the decline in Commerzbank’s investment banking, it may be time for one last risky bet.