When the champagne corks popped on Friday morning to announce Netflix’s $82.7 billion acquisition of Warner Bros., the mood in the C-suite was jubilant. Bankers cheered the return of mega-M&A, and headlines heralded the birth of a new “Streaming Sovereign.”

But as the weekend wore on, the euphoria on Wall Street began to curdle into anxiety. By Monday morning, the narrative had shifted. Analysts are slashing price targets, downgrading ratings, and asking a question that management struggled to answer on their investor call: How exactly does this massive debt pay for itself?

While Netflix frames this as a victory lap, a closer look at the balance sheet reveals a high-stakes defensive play that has left investors staring at a mountain of leverage and a regulatory minefield.

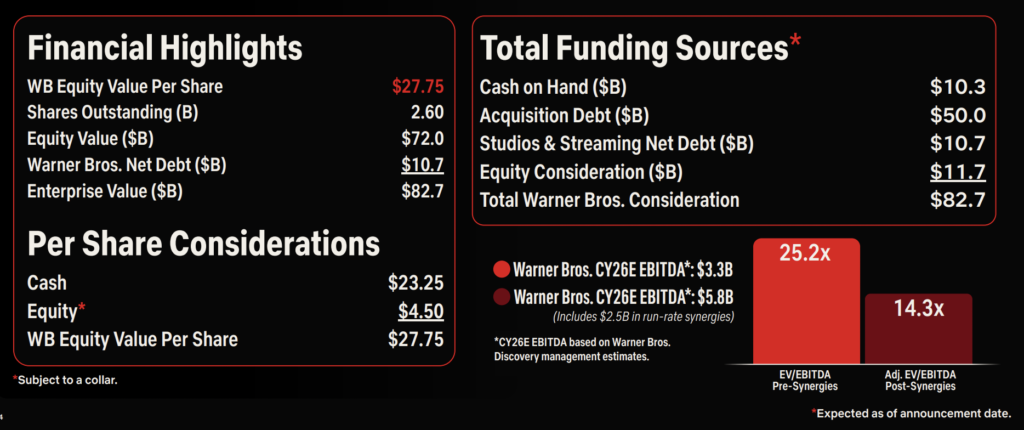

The $82 Billion Credit Card Bill

The most immediate shock is the sheer scale of the financial burden. To fund the cash portion of the deal ($23.25 per share), Netflix has secured a staggering $59 billion bridge loan. According to Oppenheimer analysts, this could push the company’s pro forma debt load to an estimated $76 billion.

For a company that spent the last decade painstakingly cleaning up its balance sheet to achieve investment-grade status, this is a abrupt U-turn. CFO Spence Neumann admitted on the call that leverage would be “elevated at closing,” with a promise to deleverage within two years.

But the market is skeptical. Taking on tens of billions in new debt at 2025 interest rates is a heavy anchor. It transforms Netflix from a nimble tech growth stock into a debt-laden media conglomerate—the very structure that dragged down Warner Bros. Discovery in the first place.

The “Synergy” Math Doesn’t Add Up

To justify an $82 billion price tag—a significant premium over WBD’s recent trading value—you need massive cost savings or explosive revenue growth. The math presented so far is underwhelming.

Netflix management identified only $2.5 billion in annual cost synergies, largely from cutting “duplicative” roles and merging tech stacks. As Morningstar analysts noted, paying such a premium for a company with overlapping subscribers makes it “difficult for Netflix to realize the full value” of the investment.

When pressed by Morgan Stanley analyst Ben Swinburne on how the deal creates value beyond just “running the businesses as is,” management pivoted to vague buzzwords. Co-CEO Greg Peters spoke of a “flywheel” where better content leads to more engagement, which leads to retention.

But “better engagement” is a soft metric for a hard debt payment. As one analyst noted, there is “no free lunch”. If Netflix keeps HBO separate and maintains theatrical releases as promised, where do the efficiencies come from? The only remaining lever is pricing power—raising subscriptions. And that leads directly to the next problem.

The Regulatory Paradox

Netflix is now trapped between two opposing masters: its shareholders and antitrust regulators.

- To Shareholders: The deal is a “defensive moat” that creates a monopoly-like position, allowing them to raise prices and cut content spend over time to pay down that $76 billion debt.

- To Regulators: The deal is “pro-consumer,” offering “more choice and value” and “lower prices” (implicitly, through efficiency).

They cannot both be true. If the deal lowers prices and increases output, it won’t generate the cash needed to service the debt. If it raises prices and restricts output (to save money), it validates the “anti-monopoly nightmare” scenario painted by some policymakers.

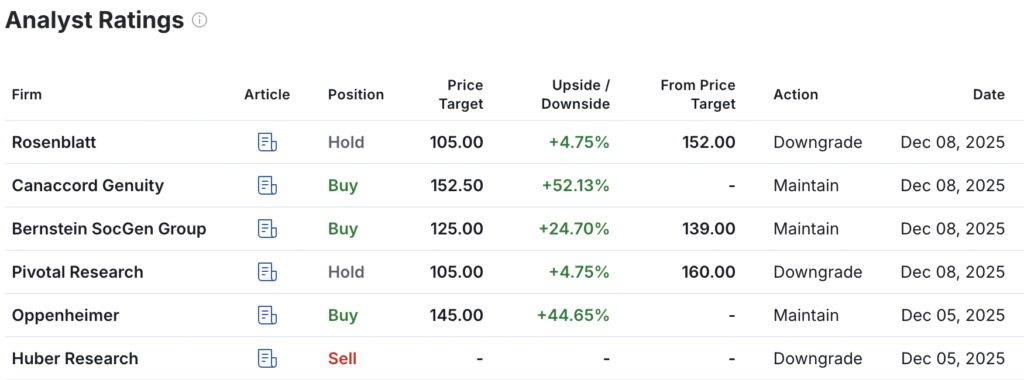

This contradiction has triggered a wave of caution. Pivotal Research downgraded Netflix stock to Hold, slashing their price target from $160 to $105, specifically citing regulatory risk and the high valuation. The fear is that the $5.8 billion breakup fee—money Netflix pays if the deal is blocked—turns this gamble into an expensive failure.

Defense, Not Offense?

Perhaps the most telling moment of the investor call came when Bernstein analyst Laurent Yoon asked if the deal signaled a lack of confidence in Netflix’s organic growth. He noted that “engagement has become a question” over the past year.

Management denied this, claiming the deal accelerates an already healthy business. But investors are wondering if this is actually a defensive move to insulate against the real threat: YouTube and social media. As traditional TV collapses, Netflix may have realized it cannot compete for time against TikTok and YouTube with just its own library. It needed Warner’s 100-year catalog to build a wall high enough to keep subscribers from churning out.

Analysts’ View

The rift on Wall Street regarding the deal’s viability widened immediately on Monday morning. Pivotal Research and Rossenblatt led the bearish charge, downgrading Netflix from “Buy” to “Hold” and aggressively slashing its price target from $160 and $152 to $105. In a note to investors, Pivotal cited “substantial regulatory risk” as the primary driver for the downgrade, arguing that the high valuation and the likelihood of a protracted antitrust battle make the stock dead money for the foreseeable future. For Pivotal, the $5.8 billion breakup fee looms larger than any potential synergy, effectively capping the stock’s upside until regulators weigh in.

Conversely, Oppenheimer maintained its “Outperform” rating with a price target of $145, taking a more pragmatic view of the company’s ballooning balance sheet. While acknowledging the sheer scale of the new leverage, Oppenheimer analysts argued that the debt load is “manageable,” estimating it at approximately 4x net debt/EBITDA. Their thesis rests on the belief that Netflix’s cash-generation engine is robust enough to service this debt rapidly, viewing the acquisition not as a financial burden, but as a necessary lever to secure long-term dominance in a consolidating market.

Conclusion

The “optimism” of Friday has faded into the cold reality of Monday. Netflix has bet the farm on a legacy studio model it once disrupted.

If the deal clears, Netflix becomes the undisputed King of Media—but one burdened by a peasant’s debt. If it collapses, Netflix loses $5.8 billion and is left with no “Plan B” for growth in a saturated market.