Indra Sistemas (BME: IDR) was added to our portfolio not on the basis of a specific regulatory event, but due to a favourable convergence of political and macroeconomic factors.

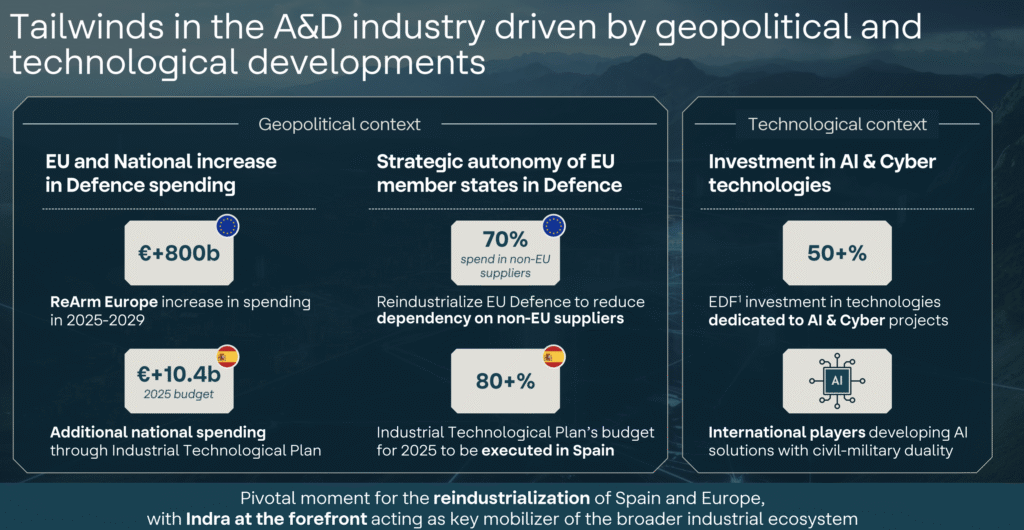

The Spanish technology and defence group has delivered strong growth, driven primarily by its defence division, as European governments accelerate military spending in response to rising geopolitical tensions. Over the past year, Indra has been strategically pivoting from civil to military projects, positioning itself to benefit from substantial increases in European defence budgets — including the €800 billion “ReArm Europe” initiative running through 2029 and an additional €10.4 billion allocated for 2025 alone.

European and Spanish Political landscape

As noted above, Europe plans to allocate €800 billion to rearm the continent. While industry leaders such as Rheinmetall, Leonardo and Thales will inevitably capture a significant share of this investment, smaller players — including Hensoldt, Prysmian and Indra — are also well positioned to benefit.

In its mid-year results, Indra underscored how the EU’s strategic autonomy agenda is accelerating defence reindustrialisation. The company highlighted that approximately 70% of current EU defence spending still flows to non-EU suppliers — a gap that presents substantial opportunities for European defence contractors like Indra.

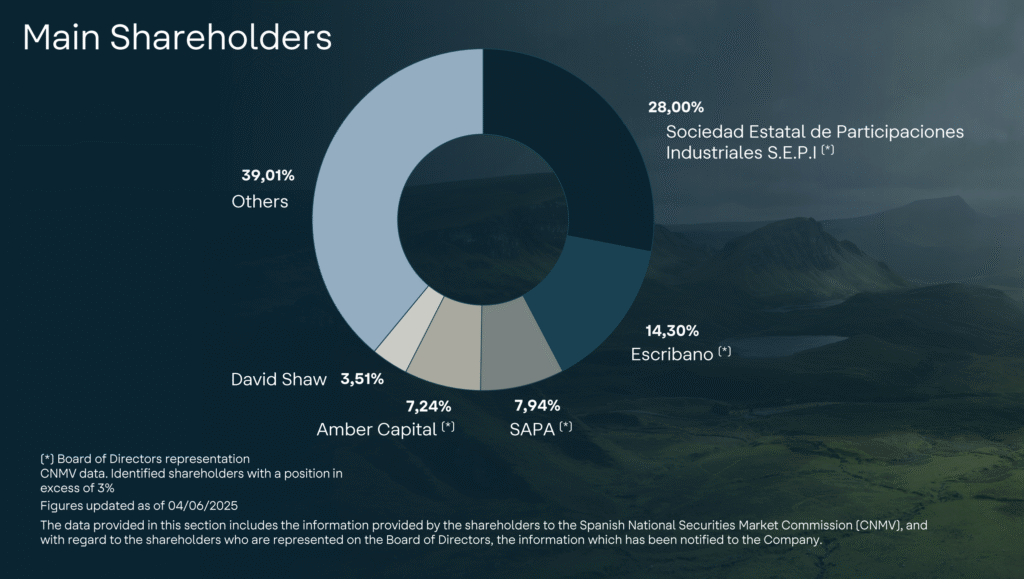

What differentiates Indra from its peers is the degree of direct state backing it enjoys. The Spanish government is not merely supportive — it is the company’s largest shareholder and is actively shaping Indra’s strategic positioning.

This backing has translated into several tangible advantages: regulatory clearance for multiple acquisitions of smaller defence companies, privileged access to public procurement across key defence programmes, and, most recently, exclusive access to €4.2 billion in state loans at a 0% interest rate. Few — if any — European defence contractors benefit from such a concentrated alignment of industrial policy and ownership.

Company Analysis

Indra operates across four strategic business lines:

- Defence

- Air Traffic Management

- Space

- Minsait — its high-technology division focused on AI, cybersecurity and digital transformation

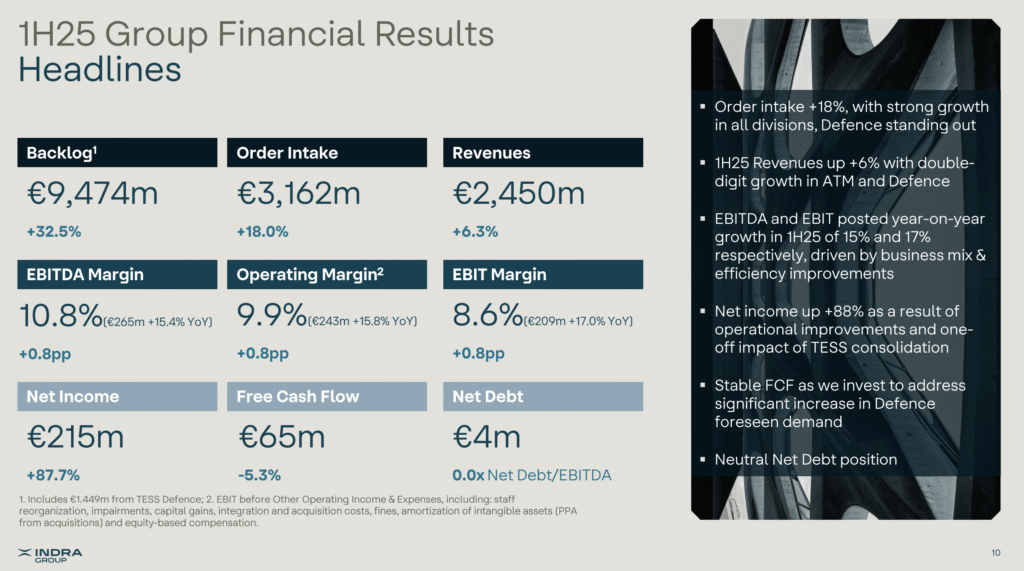

The company has reported revenue growth across all segments, but — as expected — the defence division is driving the outperformance. Net order intake in this segment has more than doubled previous expectations for 2025, reflecting exceptional demand momentum.

Profitability improved across the board in the first half of 2025, with EBITDA margin reaching 10.8% (up 0.8 percentage points), operating margin at 9.9% (up 0.8pp), and EBIT margin at 8.6% (up 0.8pp). Free cash flow remained relatively stable at €65 million (-5.3%), as the company continued investing to address increased demand in the defense sector. But these numbers are expected to improve further in 2025.

Notably, Indra maintained a neutral net debt position with just €4 million in net debt, representing a 0.0x Net Debt/EBITDA ratio, providing the company with significant financial flexibility for future investments and potential acquisitions.

A key highlight of Indra’s presentation was the launch of IndraMind, a new division focused on advanced AI and cybersecurity solutions with both civil and military applications. The company aims to build a sovereign, advanced AI platform to serve Spanish and European institutions and private companies.

IndraMind has ambitious revenue targets, aiming to reach €300 million in 2025, €700 million by 2028, and over €1 billion by 2030. The division will gradually shift from predominantly civil applications (90% in 2025) to a balanced portfolio (50% civil, 50% military by 2030).

Looking ahead, Indra confirmed its 2025 financial guidance, targeting revenue exceeding €5,200 million, EBIT above €490 million, and free cash flow over €300 million. The company expressed confidence in meeting both its 2025 guidance and 2026 Strategic Plan targets, citing its strong order backlog and favorable industry trends.

With a strong financial position, growing order backlog, and strategic initiatives like IndraMind, Indra appears well-positioned to capitalize on increased European defense spending and technological investments in AI and cybersecurity. However, the company will need to navigate challenges including supply chain optimization, geopolitical uncertainties, and the need for continuous innovation to maintain its competitive edge.

Valuation

We added Indra to our portfolio at €35 per share. At the time of writing, the stock is trading at approximately €43. Most analysts remain bullish, with price targets ranging from €44 to €48, although some have adopted a more conservative stance, placing fair value closer to €41–45.

In our own valuation exercise — using earnings-based multiples — we considered the current earnings per share (EPS) of €2.15, but applied a PER of 25 instead of 20 to reflect our view that the market is undervaluing the stock. Under this conservative scenario, we derived a price range of €53 to €62, suggesting meaningful upside potential.