The proposed acquisition of UniFirst by Cintas for $5.5 billion is as strategically intuitive for the entities involved as it is provocative for antitrust regulators. From a corporate perspective, the deal represents the final stage of a decades-long consolidation trend. By bringing the industry’s first and third-largest players under a single corporate structure, Cintas is betting on the efficiencies of a consolidated route network and substantial cost synergies; however, regulatory headwinds threaten to derail the transaction.

Deal Rationale and Regulatory Headwinds

In a logistics-heavy sector, comprising the supply of uniforms and facility services to businesses across North America, profitability is primarily driven by “stop density,” or the number of service calls a driver can execute per mile. Cintas operates more than 400 facilities across North America, while UniFirst maintains approximately 270 service locations. While Cintas possesses a more pervasive reach into rural jurisdictions, UniFirst’s infrastructure is heavily concentrated in major metropolitan markets characterized by high industrial density.

The market overlap between Cintas and UniFirst is extensive, spanning virtually every major industrial and commercial hub in North America. Both companies operate as route-based service providers, utilizing similar logistical paths to service identical client demographics, including automotive shops, healthcare facilities, manufacturing plants, and restaurants.

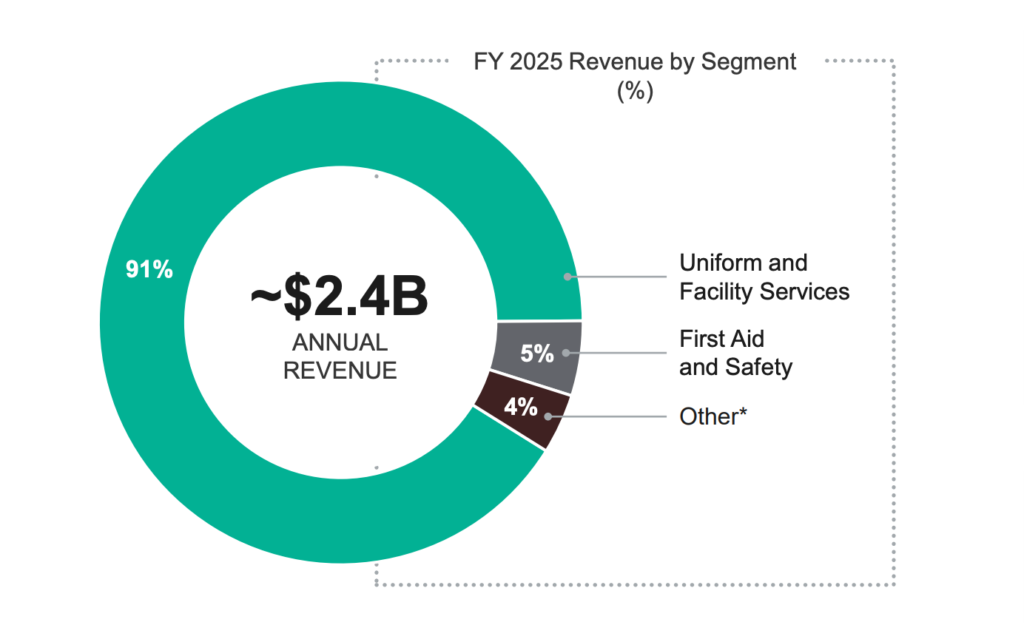

UniFirst Revenue

By merging these networks, the combined entity can eliminate redundant routes. Rather than two vehicles traveling 10 miles to service one customer each, a single vehicle can service both, significantly reducing fuel, maintenance, and labor expenditures.

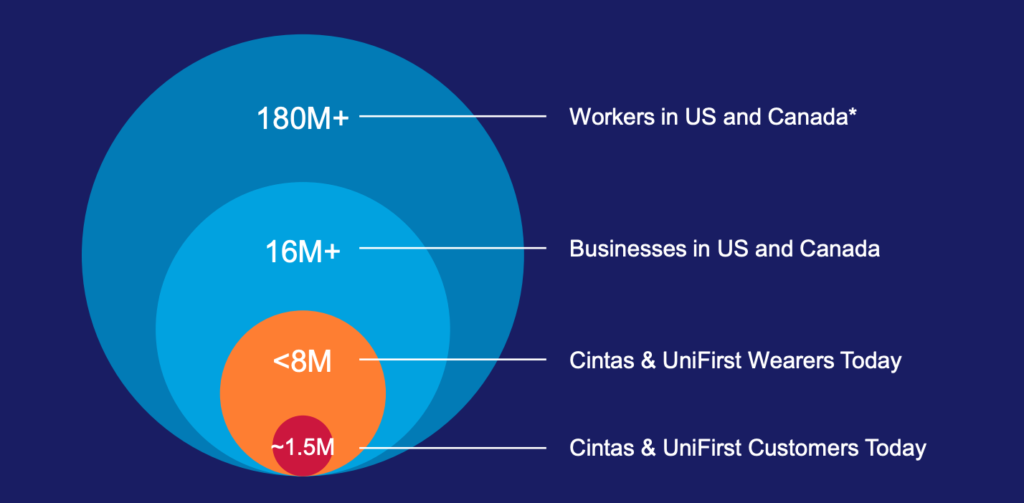

However, a combined entity would control an estimated 45% to 50% of the total North American market for uniform rentals and facility services. This scale creates a “moat” nearly insurmountable for regional competitors. When an organization can offer a national contract covering thousands of locations with a single billing point and uniform service standards, smaller independent laundries are effectively excluded from the procurement process, leaving only Vestis (formerly Aramark) as a viable national alternative.

Due to this significant overlap, the Federal Trade Commission (FTC) is expected to scrutinize specific local markets where Cintas and UniFirst are the primary dominant players. In mid-sized municipalities where a third competitor, such as Vestis or Alsco, lacks a presence, the merger could effectively establish a local monopoly.

Antitrust Hurdles

The regulatory environment in 2026 differs markedly from the landscape that permitted Cintas to acquire G&K Services in 2017. Antitrust regulators currently view “3-to-2” mergers with high skepticism. Within the national uniform rental market, the “Big Three” have historically consisted of Cintas, Vestis, and UniFirst.

If Cintas (holding approximately 35% market share) absorbs UniFirst (approximately 14%), the combined entity would control nearly half of the North American market. Applying the Herfindahl-Hirschman Index (HHI), a standard metric for market concentration, many local markets will experience “Deltas,” or increases, that far exceed the 100-point threshold for a regulatory challenge. In hubs such as Boston or Chicago, the HHI could spike by 800 to 1,000 points, creating a “highly concentrated” market presumed illegal under current guidelines.

The FTC’s inquiry will likely center on the “National Accounts” segment. Large-scale enterprises require providers with a geographic reach that local independents cannot replicate. By reducing the “Big Three” to a “Big Two,” the merger potentially fosters a duopolistic environment where Cintas and Vestis have diminished incentives to innovate or compete on pricing. Furthermore, the FTC could also examine “conglomerate power”—the capacity of a dominant entity to leverage its uniform market share to penetrate related sectors such as first aid, fire protection, and tile cleaning, thereby marginalizing specialized competitors.

A secondary complication exists in niche markets. UniFirst maintains a dominant position in nuclear and cleanroom garments, a specialized national market with virtually no substitutes. If no viable alternative buyers exist for these specialized divisions, Cintas may be unable to execute an effective divestiture. If the FTC concludes these critical niche industries would be left without competition, that factor alone could suffice to block the $5.5 billion merger.

Divestiture vs. Structural Block

Cintas management is evidently cognizant of these hurdles, as indicated by the $350 million termination fee guaranteed to UniFirst should the deal be blocked. To secure approval, Cintas will likely propose a series of divestitures. However, for a divestiture to be deemed “pro-competitive,” Cintas must identify a buyer capable of assuming UniFirst’s market position rather than merely selling assets to fragmented local firms.

Management would likely seek to “level up” an existing player, most notably Alsco or Prudential Overall Supply, to ensure they possess the national footprint required to bid on major corporate contracts (e.g., Amazon, FedEx, or national healthcare chains) currently serviced by UniFirst.

The FTC has become increasingly wary of “cherry-picking” divestitures, wherein a firm retains premium clients while offloading inefficient routes to rivals. Consequently, regulators will likely mandate the sale of “stand-alone business units”, entire regional networks including plants, management, drivers, and the underlying customer base, as a functional package.

Alsco, as the largest privately held entity in the industry, remains the most “FTC-friendly” prospective buyer. If Alsco agrees to acquire the 20% to 30% of branches Cintas may be required to shed, the probability of regulatory clearance increases.

The alternative remains a formal suit by the FTC to block the transaction. If the Commission determines that the projected synergies are derived primarily from the reduction of competition rather than operational optimization, it will argue that structural harm cannot be mitigated by asset sales. This places Cintas in a precarious financial position: the UniFirst routes are necessary to justify the $310-per-share premium, but extensive court-mandated divestitures diminish the deal’s accretive value for Cintas shareholders.

The North American Front: Canada and Labor

The merger faces two additional regulatory “wildcards.” The first is Canada, where UniFirst’s “Canadian Linen” brand is a dominant market leader. The Competition Bureau of Canada has recently repealed the “efficiencies defense,” which previously allowed anti-competitive mergers if they resulted in significant corporate cost savings. In high-density markets like Southern Ontario, the Bureau may demand divestitures that significantly impair the value of the Canadian acquisition.

The second wildcard is the “Labor Monopsony” argument. Within the 2026 regulatory framework, the impact on the workforce is weighted alongside the impact on consumers. Cintas and UniFirst are the two largest employers of route drivers and laundry technicians in numerous regions. A merger reduces the “outside options” for these employees, potentially depressing wage growth. Both the Department of Justice (DOJ) and the FTC have signaled their intent to challenge mergers that significantly consolidate a firm’s power over its labor pool.