In early 2025, the Polish bank announced plans to merge with insurer PZU to create a new integrated banking–insurance group. If completed, the transaction would release substantial capital for the bank, which could then be allocated to dividends, new lending, or further acquisitions

In our view, the restructuring carries some political risk but is still likely to go through. Financially, Bank Pekao remains in strong shape, meaning that even an adverse outcome would have limited impact on its overall stability.

The stock recently took a hit after the Polish finance minister announced plans to raise the corporate tax on banks. The tax proposal has not yet been approved, but since it would affect the entire sector equally, Pekao’s current share price (around PLN 180) may represent an attractive entry point.

REGULATORY EVENT

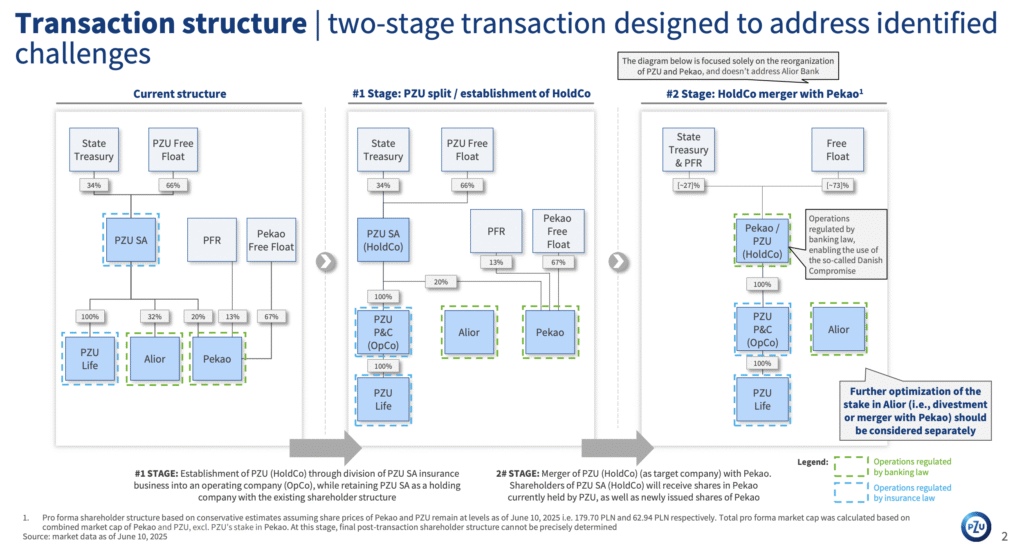

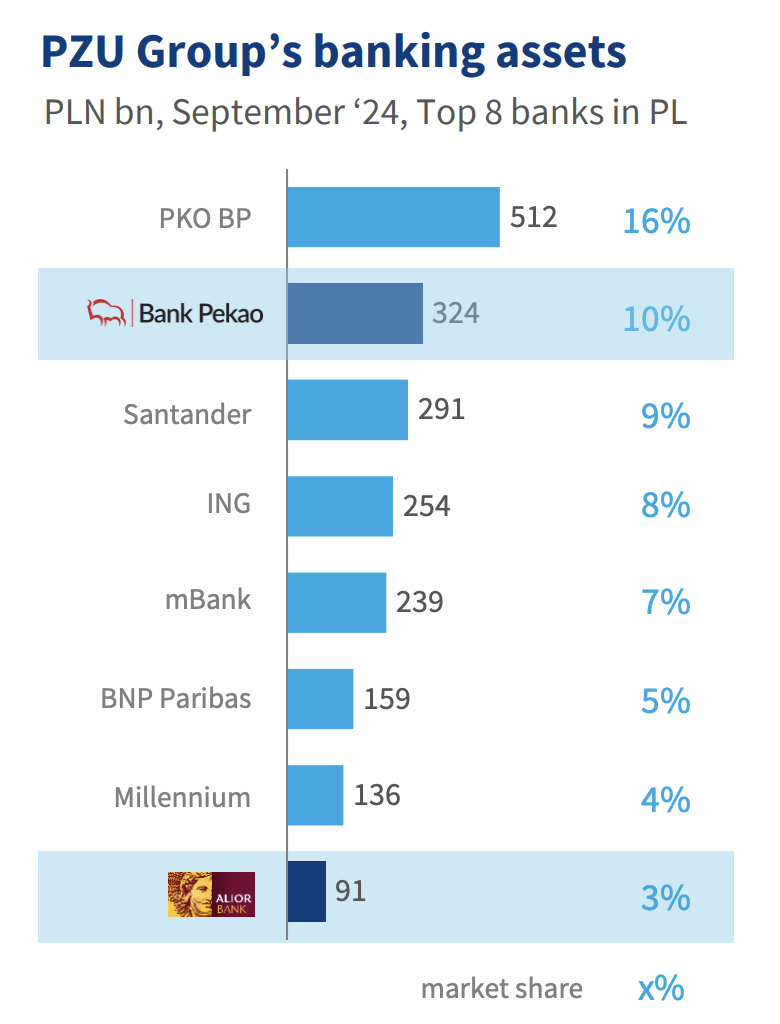

At the core of this transaction is a complex multi-step operation. PZU, currently Poland’s largest insurer and a major shareholder in both Bank Pekao (approximately 20%) and Alior Bank (31.91%), will be divided into two entities: a holding company and an operational insurance unit.

Simultaneously, PZU plans to sell its stake in Alior Bank to Bank Pekao. This means that while PZU as a legal entity exits the shareholder structure of both banks, the overall control remains consolidated under the Pekao umbrella.

The proposed transaction is scheduled for completion by June 30, 2026, pending a series of regulatory, legislative, and corporate approvals. However, the parties suggested that by end of 2025, they will have a clearer view on whether the necessary regulatory approvals will be achieved.

From Insurance-Led to Bank-Led Control

Under the Bank Pekao-PZU restructuring plan, Pekao will absorb the holding company, effectively folding PZU’s holdings under Pekao’s umbrella while maintaining state control through the State Treasury and PFR.

This deal explicitly makes Pekao, not PZU, the operational and strategic leader, in part due to legal requirements, and in part to use the Danish compromise, a legal trick that favour banks’ acquisitions of insurance companies.

Legal Amendments: Close contact with regulators

During a recent investor conference, the companies reassured shareholders that the government does not oppose the restructuring and they continue implementing legal changes. In fact, they noted that the Ministry of Economy is supportive of the plan and has encouraged the parties to use the excess capital generated by the transaction—potentially up to 20 billion zloty (around €4 billion)—to help stimulate the Polish economy, particularly as EU funds begin to taper off.

However, Bank Pekao’s CEO also acknowledged that the election of a new Polish president who is openly at odds with the government could increase the likelihood of vetoes on legislation, potentially complicating the policy environment. He also stated that if the legislative process goes differently than expected, they will look for new solutions.

Polish insurance law currently does not allow an insurer to split its operations in the way that banking law permits, making this the most critical legal change required for the restructuring to proceed. Additionally, technical amendments to banking regulations will be needed to enable the transfer of certain assets under the new structure.

There are also technical aspects that need to be changed to allow a seamless transfer of employees between entities, but these are considered minor hurdles. PZU’s management has indicated that conversations with regulators, including the Polish Financial Supervision Authority, have been constructive. The Memorandum of Understanding between Pekao and PZU emerged after intensive discussions with regulators, aligning the restructuring plan with supervisory and policy objectives.

Therefore, while the legal amendments are subject to parliamentary approval both PZU and Pekao remain confident that the necessary changes will be enacted in time to allow the restructuring to close as planned in the second quarter of 2026.

What the Danish Compromise Unlocks

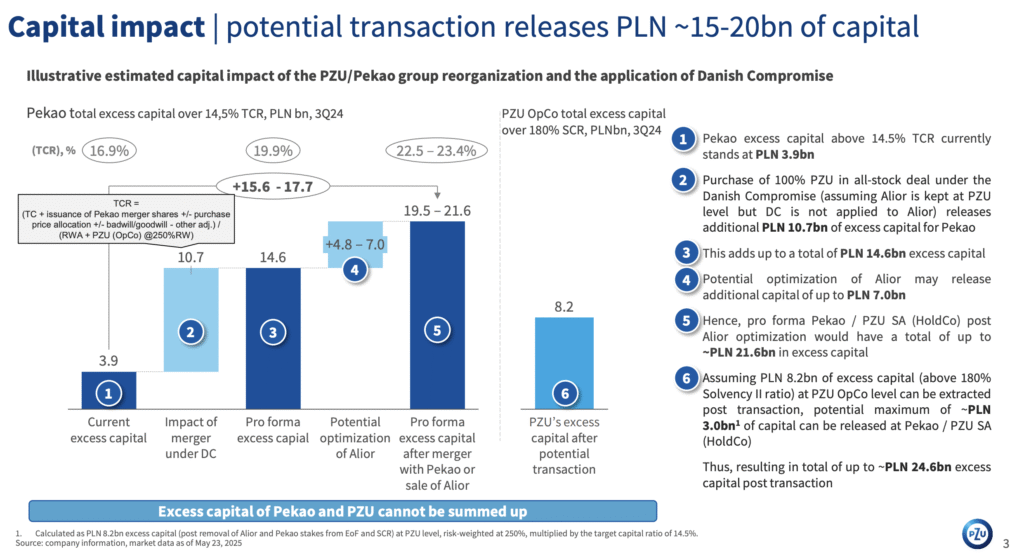

The Danish compromise is the cherry on top for this operation. The “Danish Compromise” is an EU regulation that allows European banks, under certain conditions, to risk-weight their insurance holdings instead of fully deducting them from their own capital. This means banks don’t have to reduce their capital reserves as much when they own insurance companies, making it potentially more appealing for banks to acquire or merge with insurance businesses.

The restructuring will enable Pekao to unlock PLN 15–20 billion in excess capital, providing significant room for strategic initiatives. This capital can be used for credit expansion, for selective mergers and acquisitions within Poland’s banking and insurance landscape or to support maintaining an attractive dividend policy, which currently stands at 9.7% yield

However, the transaction will require the issuance of new Pekao shares to absorb PZU’s holding company, leading to dilution for existing shareholders. While management has expressed its intention to maintain a payout ratio of at least 50-75 percent of net profit, investors should prepare for the possibility that per-share dividends may temporarily decrease despite the bank’s enhanced capital position.

COMPANY ANALYSIS

Solid Profits and Resilient Polish Economy

This restructuring takes place in a resilient Polish macroeconomic environment as Fitch has pointed out. Despite geopolitical uncertainty in Europe, Poland’s economy continues to demonstrate stability, driven by strong domestic demand, steady employment, and a controlled inflation trajectory.

This context underpinned Fitch’s recent upgrade of Pekao’s rating to BBB+ with a stable outlook. The agency cited Pekao’s solid capital buffers, conservative risk profile, and strong deposit-based funding as key strengths, noting that the restructuring, while complex, should not undermine Pekao’s risk management discipline or its capacity to maintain stable operations. This upgrade provides confidence that Pekao can handle this structural transition while continuing to deliver for shareholders but the rating agency also warns of execution risks and the possibility to review this rating but overall, the report is overly positive.

Bank Pekao delivered strong second-quarter results, with net profit up nearly 13% year-on-year to PLN 1.6 billion, underpinned by solid growth in lending and resilient margins. Loan volumes rose 6% from a year earlier—driven by double-digit growth in cash loans and SME financing. The cost-to-income ratio improved to 33%, and return on equity held at a healthy 20%.

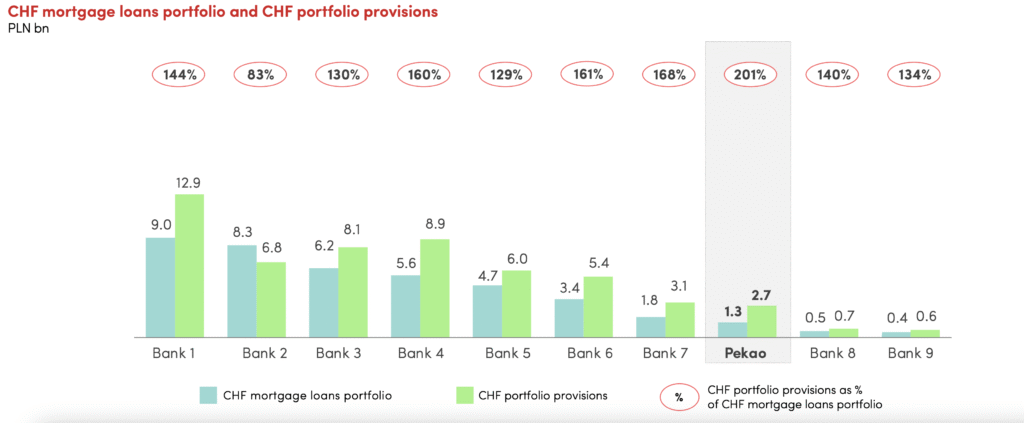

The bank also reported further progress in reducing its already limited exposure to Swiss franc mortgage litigation, with roughly three-quarters of the portfolio either repaid or converted to złoty. Notably, it has set aside provisions exceeding twice the value of its remaining CHF mortgage loans, underscoring a conservative approach to managing this legacy risk.

Alior Bank: In or Out, either way is good

Alior Bank’s future -who also reported good 2Q results- is yet an unresolved component of Pekao’s post-restructuring landscape. PZU currently holds a controlling stake in Alior, and its treatment will significantly influence Pekao’s future capital flexibility.

Integrating Alior would increase Pekao’s market share, particularly in SME and consumer lending, and further strengthen its position in the Polish banking sector. However, it would also consume a portion of the capital the restructuring aims to unlock (around 7 billion zloty), potentially stretching prudent capital ratios and limiting the bank’s ability to pursue other strategic opportunities. Alternatively, a sale of Alior could simplify Pekao’s structure and release additional capital, while maintaining the status quo would preserve flexibility until market conditions are clearer.

A potential future integration of Alior into Pekao would likely attract attention from Poland’s Office of Competition and Consumer Protection, especially in lending markets, but given the highly fragmented banking landscape, that operation is unlikely to raise competition concerns.