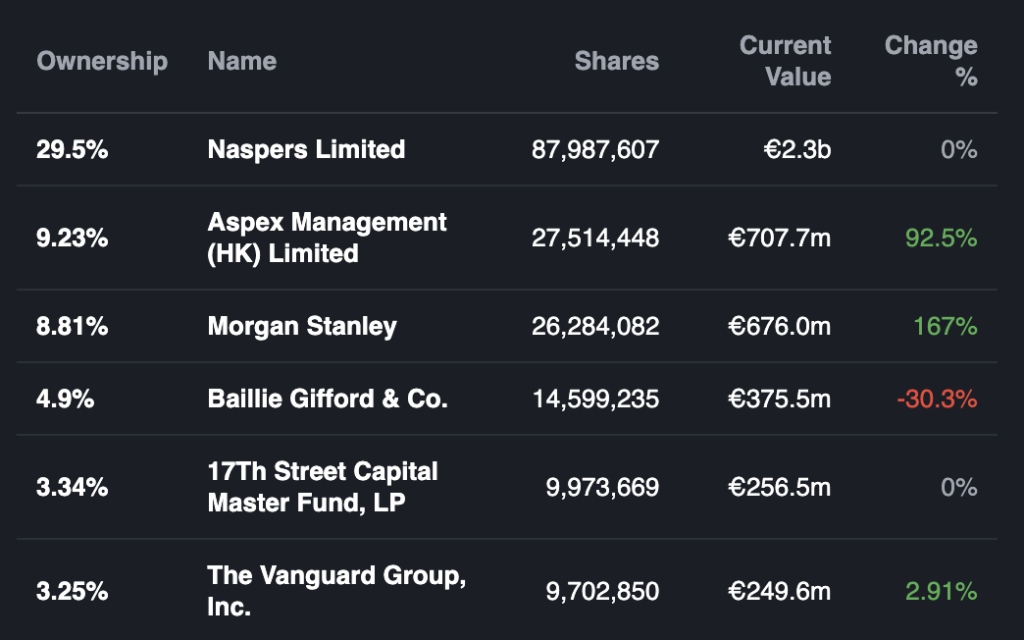

Dutch technology investor Prosus is reportedly considering selling part of its shareholding in German food delivery company Delivery Hero to Hong Kong-based investment firm Aspex Management. According to a Bloomberg News report citing people familiar with the matter, the potential transaction could involve the sale of roughly a 10% stake in the Berlin-based company.

Prosus (via Naspers) is currently the largest shareholder in Delivery Hero (around 29%), one of Europe’s leading online food delivery platforms. If completed, the sale would mark a change in the company’s shareholder structure and it would position Aspex as the largest shareholder, a helpful position to support its plan to depose the CEO.

Delivery Hero’s Top Shareholders

The EC’s “Hidden” Deadline: Predicting the Prosus Divestiture

When the European Commission cleared Prosus’s acquisition of Just Eat Takeaway (JET) in August 2025, the focus was on the birth of a European tech champion. However, the “price” of that approval was a strict structural remedy: Prosus had to divest part of its stake in Delivery Hero to ensure it was no longer the company’s largest shareholder. We flagged to our clients in the February Inner Circle that this created a “forced seller” dynamic with a looming August 2026 deadline. Today’s news that Prosus is offloading a 10% stake to Aspex Management is not a surprise, it is the inevitable conclusion of a regulatory clock that has been ticking for months.

Aspex’s Bold Move: Growth Strategy or Missed Due Diligence?

By acquiring this 10% stake (probably a bit more than that), Aspex Management is effectively becoming the lead voice in Delivery Hero’s future and it does so at a very attractive price. For Prosus, the timing of this sale is a tactical necessity to satisfy Brussels, but for Aspex, it is a strategic window. They are buying into a company where they have already publicly called for a change in leadership and a radical overhaul of the capital allocation strategy. However, while the market sees this as a “turnaround” play, the actual financial health of the company remains shielded behind accounting adjustments.

A critical question is why Prosus sells now at €15/share, when just a few months ago was €25/share? Didn’t have good financial analysts that saw this decline coming? It was not a secret that Delivery Hero was struggling, the second largest shareholder was not happy, and the whole delivery food industry is under pressure.

Then it came the “profit”.

The “Adjusted” Mirage: Why Aspex Needs Forensic Due Diligence

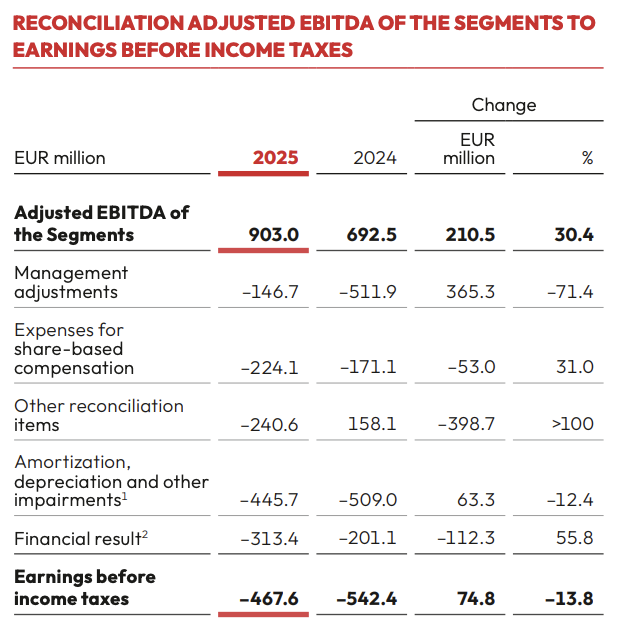

Just on March 26, one day before the Bloomber news, Delivery Hero reported record profits.

On the surface, Delivery Hero’s latest report of a 30% jump in Adjusted EBITDA (€903 million) suggests a business that has finally turned the corner. But as we have consistently warned, the gap between “Adjusted” performance and “Net” reality is widening. Management’s 2026 guidance specifically excludes “extraordinary cash outflows” related to legal matters (and other risks). In reality, Delivery Hero is currently absorbing a €329 million EU antitrust fine for “no-poach” cartels (already accounted in 2024) while simultaneously fighting a massive regulatory reclassification of its rider workforce in Spain. This “Spain Rider” risk alone represents a potential €700 million liability that could evaporate the very cash flow investors are currently betting on.

To make things worse, the company is getting a new loan to pay old bonds. In other words, refinancing old debt with new debt. For some investors, the picture is Delivery Hero got 30% boost in profits and a new landscape, but for others, perhaps including Prosus who is selling low, the financial situation may be less rosy than the record profits announced.

Details of the potential share sale by Prosus, including the value and timing of the transaction, have not been publicly confirmed. Reuters reported that it was not immediately able to independently verify the Bloomberg report. Neither Prosus, Delivery Hero nor Aspex Management have publicly commented on the reported discussions, and it remains uncertain whether the negotiations will result in a completed transaction. But Prosus needs to sell that stake of Delivery Hero before August 2026.

The Lesson for M&A Professionals

The Prosus-Aspex transaction proves that in 2026, a purely legal or purely financial analysis is no longer sufficient. If you only tracked the merger filing, you missed the hidden financial risks (and other legal risks) If you only tracked the stock price and the EBTIDA, you missed the legal obligations imposed by the European Commission. This deal is a masterclass in why modern due diligence must be forensic: it’s about identifying where a regulatory deadline creates a price advantage for a buyer, but also where “Adjusted” financial reporting masks a structural legal threat.

If you want to spot opportunities and red flags before the market catches up, book a call with us.