AT&T is leaving Mexico, and Grupo Televisa (Izzi/Sky) is the frontrunner to acquire these assets. A potential acquisition by Televisa will trigger a complex antitrust review due to the intersection of market convergence, preponderance status, and historical regulatory precedents.

But in all honesty, there aren’t many suitors, and two strong players (Televisa and América Movil) are better than just one strong player (América Movil). Therefore, the question is not whether the deal will be approved, but what conditions regulators may impose on Televisa to protect consumers and Mobile Virtual Network Operators (MVNOs).

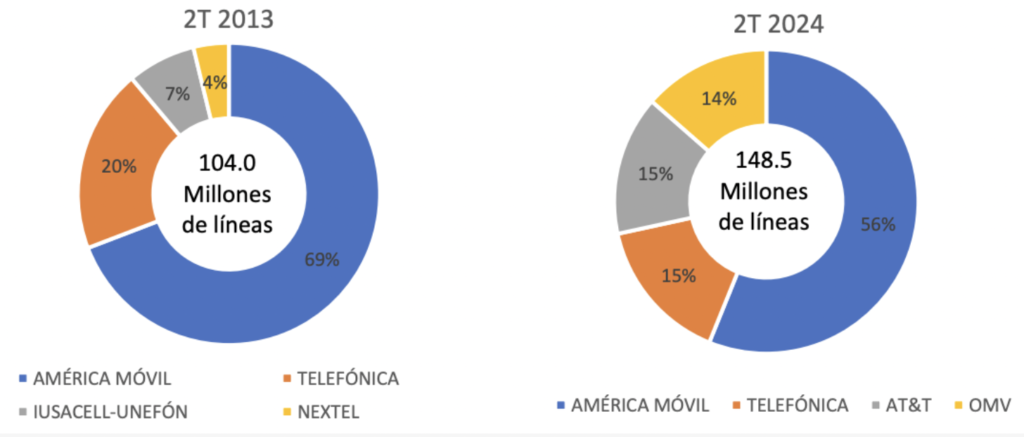

Market Share Mobile Phone Lines (in millions)

The Rise of a Convergent Giant

Televisa’s interest in AT&T Mexico represents the final piece of its “quad-play” puzzle. By merging its dominant Pay-TV (Sky) and fixed broadband (Izzi) assets with a national 5G mobile network, Televisa can create a seamless ecosystem of content and connectivity.

The strategic logic is clear: Convergence. In a market where digital consumption is soaring—projected to reach 120 million mobile internet subscriptions by the end of 2026—owning the “pipe” and the “program” is the only way to challenge the hegemony of Carlos Slim’s América Móvil.

This isn’t a plain telecom exit—it’s a convergence play with preponderance in the background. If Televisa (already preponderant in broadcasting) adds AT&T Mexico’s mobile network to Izzi/Sky, regulators will look past headline market shares and focus on leverage: the ability to tie content and connectivity into quad-play bundles, cross-subsidize pricing, and use exclusivity or distribution tactics that raise switching costs and squeeze narrower rivals. And if the acquired network remains the wholesale “host” for MVNOs or other players, the case becomes even sharper: Televisa could end up competing at retail while sitting on competitors’ inputs—forcing scrutiny around non-discrimination, quality, wholesale pricing, and firewalls for sensitive commercial data—even if the broader narrative is that a second scaled challenger may be preferable to a one-horse race dominated by Telcel.

However, this convergence also brings antitrust and telecommunication concerns:

- Fixed-Mobile Convergence & Bundling: Televisa (Izzi) is already a dominant force in fixed services (Internet and Pay TV). Acquiring AT&T Mexico would allow it to scale “quad-play” offers. This raises risks of cross-subsidies and aggressive bundling strategies that could increase switching costs for consumers or foreclose the market to smaller rivals with narrower portfolios.

- Preponderance & “Conglomerate Effects”: While América Móvil (Telcel) remains the “preponderant agent” in the sector, regulators may still scrutinize whether a second large-scale convergent player would increase competitive pressure (a pro-competitive effect) or create “foreclosure” risks in specific niches like content, advertising, distribution, or access.

- Regulatory Track Record: The former Federal Telecommunications Institute (IFT) previously declared Televisa as having substantial market power in the restricted TV market (2020), despite subsequent litigation and court reconfigurations. The IFT has also investigated “relative monopolistic practices” regarding unbundled programming, though it ultimately decided not to issue sanctions. If the deal proceeds, Televisa should expect deep inquiries into fixed-mobile bundling, the treatment of rival distributors, and exclusivity conduct.

The “Landlord” Dilemma

The acquisition is further complicated by the likely exit of another giant: Telefónica (Movistar). Under its Transform & Grow 2026-2030 plan, Telefónica is selling its 23.5 million Mexican subscribers.

Movistar returned its spectrum years ago and operates entirely on AT&T’s infrastructure. If Televisa buys AT&T, it becomes the “Landlord of its Competitors”—nothing different than what AT&T is doing right now, but it still creates a conflict of interest that needs to be managed.

Televisa would act as the wholesale provider for Movistar and any other MVNO while simultaneously competing with them for retail customers. Since 2022, Izzi Móvil has used Altán and AT&T’s network to expand its coverage. This situation poses risks like: degradation of quality or coverage, less competitive wholesale pricing, and strategic use of sensitive data (e.g., churn rates, demand geography, and volumes) from wholesale clients to benefit Televisa’s retail arm.

What Regulators May Do

To authorize the merger, the National Antitrust Commission (CNA) and the Regulatory Telecommunications Commission (CRT) would likely demand specific conditions, but blocking the deal is unlikely:

- Mandatory Wholesale Continuity: Televisa may be forced to guarantee network access to MVNOs for at least 5–7 years.

- Information Firewalls: Preventing Televisa’s retail arm from seeing sensitive data (like churn rates) of the rivals using its network.

- Functional Separation: Keeping the “Network Operation” entirely separate from the “Sales and Content” divisions.

- Specific divestitures of assets or infrastructure (unlikely) in local segments where bottlenecks cannot be resolved through behavioral conduct alone.

An Unanswered Question

As noted in our previous analysis, Televisa’s ambition faces a harsh financial reality. The company is already digesting the Sky acquisition while its debt-to-EBITDA ratio hovers near 4.6x. How will Televisa finance this deal?

Financing such a move—estimated at over $2 billion—without increasing its net debt/EBITDA ratio (which could trigger a downgrade) would likely force Televisa to liquidate “crown jewel” assets. While the company could sell part of its 45% stake in TelevisaUnivision, doing so right before the 2026 World Cup (hosted in North America) feels like selling at the peak of the hype.

Alternatively, Televisa could also sell the remaining 51% stake in Ollamani (the company that houses Club América, the Azteca Stadium, and the gambling division PlayCity). As of January 2026, Ollamani is trading with a market cap of approximately $9.4 billion MXN (roughly $550 million USD). But this sale wouldn’t add a significant amount of cash, thus, Televisa would still need to tap additional sources.